Every week in Bridgeport, I sit with immigrant families as they divide their limited weekly earnings in two different directions. Part will pay the rent here in Connecticut. The remaining amount will be transferred back to a family member overseas.

I started a bilingual financial literacy program for these families, but many of the questions they ask me are not related to my services. Instead, they want to know how to safely transfer money to relatives living in Guatemala, the Dominican Republic, or Mexico. Economists call this kind of transfer a remittance. Together, millions of these transfers create a massive flow of capital out of wealthy nations and into lower and middle-income countries.

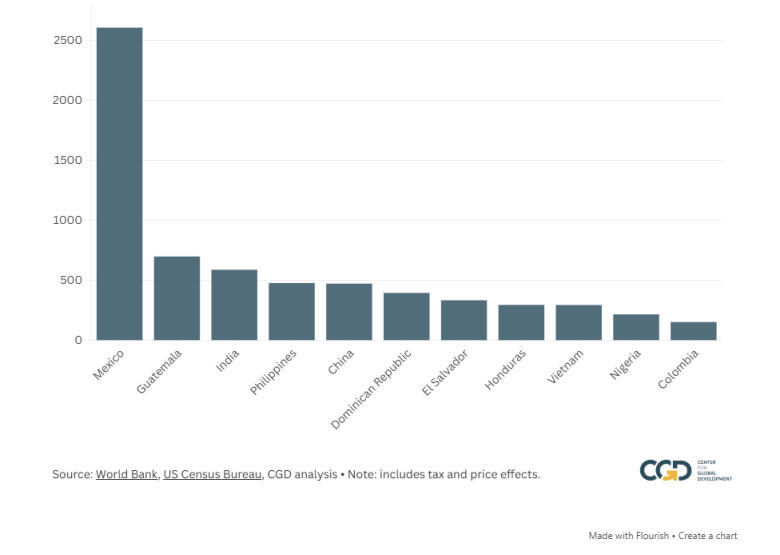

According to the World Bank, migrant workers transferred over $685 billion into low and middle income countries in 2024, a total that surpassed both foreign direct investment and international development assistance. The Inter-American Development Bank reports that Latin America and the Caribbean received approximately $161 billion in remittances during 2024, and the World Bank puts Mexico’s share at about $68 billion , making it the second largest recipient in the world.

Numbers this large become foreign policy issues. Researchers at the Overseas Development Institute found that in 2023, remittances to developing countries reached approximately $656 billion, three to four times greater than global foreign assistance, which totaled roughly $224 billion. Unlike foreign assistance, which can take months or years to arrive, remittances are paid directly to recipients and spent immediately on basic necessities such as food and medicine. They represent one of the most efficient poverty reduction programs yet developed, and no government designed it.

It should disturb anyone concerned with U.S. foreign policy that Congress has chosen to tax the money sent abroad through remittances.

As part of President Trump’s One Big Beautiful Bill Act, signed into law on July 4, 2025 , a new 1 percent excise tax was added on money sent abroad, beginning January 1, 2026. Earlier versions of the bill proposed a 5 percent tax and then a 3.5 percent tax before lawmakers settled on 1 percent. They also extended its scope to cover both citizens and immigrants. Based on data from the Center for Global Development, an estimated 48 million foreign-born individuals could be affected.

Although a 1 percent tax appears minor when expressed as a decimal, its implications are strategic. The same analysis projected that Mexico could lose over $1.5 billion per year, and that El Salvador, a country whose stability Washington treats as an important relationship, could lose the equivalent of roughly 0.6 percent of its national income. These are precisely the economies whose instability contributes to the migration that Washington says it wishes to reduce. By taxing remittances and lowering incomes in these countries, Washington will have worsened the root cause of the immigration problem while claiming to address it.

The tax also fails on its own merits. The law excludes bank transfers and payments made with U.S. issued debit and credit cards, so it falls hardest on cash transactions, the method used by people who do not have or cannot obtain bank accounts. As predicted, taxing the most transparent means of sending money pushes families toward less transparent channels, the reverse of what the tax intends. It also stacks on top of the roughly 6 percent that migrants already pay in transfer fees, about twice the 3 percent rate the United Nations set as a global development goal.

I was drawn to this issue by faith as much as economics. Catholic social teaching upholds the dignity of work and the central importance of the family, and a remittance is exactly that: money earned through one’s labor and sent across a distance out of love. To tax it is to treat an act of devotion as a loophole to be closed.

There is a superior alternative to the policy our federal government is advancing on immigration. Lower the cost of transferring money internationally. Rather than punishing the people locked out of the banking system with higher costs, give them greater access to it. And treat remittances as what they are, a development tool more effective than nearly all of the direct funding we engage in. A nation confident in its own economic strength does not need to take a cut from the money a domestic worker sends home to her mother.

I will continue to spend my days with these families in Bridgeport, helping them find ways to safely send as much of their earnings as they can. But the next time I hear someone claim that Washington is trying to address immigration at its source, I will remember the new line on that $60 transfer, and I will wonder whether anyone in the room understood what they were taxing.

Marcos Cruz lives in Fairfield.