There’s been a lot of news this week about what it will cost to buy insurance through the new marketplace created by federal health reform. But what will those prices get you?

For many people, choosing the cheapest premium will mean buying a plan with a $3,250 deductible and additional costs once the deductible is met — in many cases, 40 percent of the price of care. Buying the most expensive plan, by contrast, would mean having a $1,000 deductible and, after reaching it, paying fixed copays — $20 or $45.

There are some exceptions: People with low incomes can qualify for plans with lower deductibles — or, in some cases, no deductible — and copays as low as $5. About 95,400 of the nearly 380,000 uninsured Connecticut residents are believed to have incomes low enough to qualify for some discount on the out-of-pocket costs they’d face if they buy insurance through the new marketplace.

What’s the same, what varies

Health plans sold on the new marketplace, a health insurance exchange known as Access Health CT, must cover a set of federally defined “essential health benefits.” Each insurer offering coverage through the exchange must also sell a plan that meets a standard design set by Access Health.

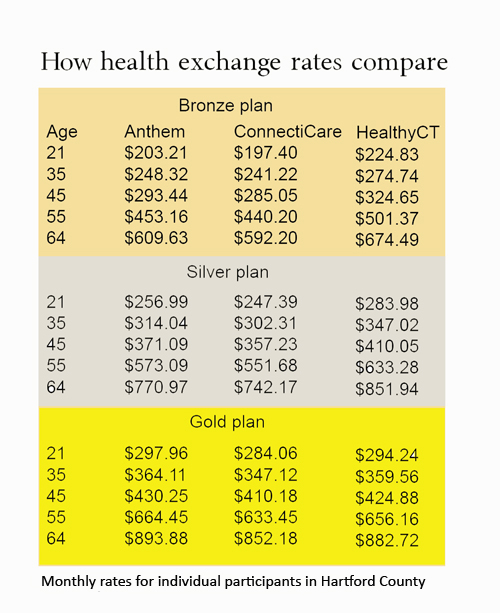

So what can vary between the plans offered by different insurance companies? The price of the plans, and which health care providers belong to an insurer’s network.

For each insurer offering coverage, customers will have a choice between three types of plans, signified by metals: bronze, silver and gold.

It’s a choice between plans that cost less upfront but require more out-of-pocket spending when getting care, and plans that cost more each month but require less cost when using medical services.

Bronze, silver, gold

If you buy a bronze plan — the cheapest available for anyone 30 and older — you’ll have a $3,250 deductible for individual coverage; it’s $6,500 for family coverage. Once you spend that much on medical care, including medication, you’ll still have to pay 40 percent of the cost for many services, including visits to specialists, outpatient hospital services, emergency room visits and lab work.

If you buy a bronze plan — the cheapest available for anyone 30 and older — you’ll have a $3,250 deductible for individual coverage; it’s $6,500 for family coverage. Once you spend that much on medical care, including medication, you’ll still have to pay 40 percent of the cost for many services, including visits to specialists, outpatient hospital services, emergency room visits and lab work.

You’ll also have to pay 40 percent of the cost of non-generic drugs. But each customer’s out-of-pocket costs will be capped at $6,250, or $12,500 for a family plan.

Silver plans have similar deductibles to the bronze ones — $3,000 for medical services, plus $400 for prescription drugs; both of those figures are doubled for family plans.

But the deductible applies to a narrower range of services, including inpatient hospitalization, outpatient procedures, and non-generic drugs. You’d pay fixed copays for office visits ($30 to see a primary care doctor for an injury or illness, $45 for a specialist), lab work and urgent or emergency care.

As with the bronze plan, your out-of-pocket costs would be capped at $6,250 for an individual or $12,500 for family coverage.

Gold plans cost the most, but people who buy them will face the lowest out-of-pocket costs. There’s still a deductible, but it’s lower: $1,000 for medical services, and $150 for prescription drugs (again, double that for family plans). As with the silver plan, the deductible applies to hospital stays, outpatient procedures and non-generic drugs. But for office visits, lab work and urgent or emergency care, you’d have fixed copays.

The maximum amount you’d pay out-of-pocket is lower too: $3,000 for an individual and $6,000 for a family.

All those figures are for health care providers in the particular plan’s network. Deductibles and cost-sharing are higher for out-of-network providers.

Lower out-of-pocket costs for some

People who earn below 250 percent of the poverty level will have another option: A silver plan with reduced out-of-pocket costs, subsidized by the federal government. That’s in addition to federal funding that will discount the cost of premiums for many exchange customers.

The typical silver plan will cover about 70 percent of a person’s medical costs, leaving the customer to pay the other 30 percent through the deductible and copays. The options available to the lower-income customers would change that split. The poorest exchange customers could buy plans that cover 94 percent of their medical costs, while others would qualify for plans that cover 87 percent or 73 percent of their costs, depending on their income.

The biggest cost reduction, the 94 percent plan, has no deductible and copays of $5 or $15 for many services. It’s available to people earning less than 150 percent of the poverty level — less than $17,234 for an individual or $35,324 for a family of four. (These are people just above the threshold for Medicaid, which, as of Jan. 1, will be expanded to cover those earning up to 138 percent of the poverty level.)

People earning between 150 percent and 200 percent of the poverty level could buy a plan that covers 87 percent of their medical costs, leaving them with a $500 deductible ($1,000 for family coverage) and $10 or $30 copays for many services.

Those earning between 200 percent and 250 percent of the poverty level would qualify for a plan with a $2,500 deductible for medical services and a $300 deductible for prescription drugs (both figures are doubled for family coverage), and $30 or $45 copays for many services.