The cost of employer-sponsored health insurance rose modestly throughout the country in 2013, but the growth was still more than twice that of wages and nearly five times higher than inflation, according to a report released Tuesday.

Even so, it was a relatively stable year for employer-sponsored health insurance — perhaps the last for a while.

“More changes are expected over the next several years as many of the more far-reaching provisions of the health reform law will take effect in 2014,” said the report, released by the Kaiser Family Foundation and Health Research & Educational Trust.

Those changes include new rules about what benefits health plans must cover, how insurance prices are set, and the creation of new insurance marketplaces that will allow individuals and employees of small businesses to select from multiple plans.

Some experts expect smaller employers to consider dropping coverage and letting their workers buy insurance in the new marketplaces, while larger employers might consider changing the way they handle benefits to give workers more choices and financial responsibility.

Meanwhile, companies are increasingly offering wellness programs aimed at improving workers health, something expected to continue as a new tax on high-cost plans looms in 2018.

What it costs

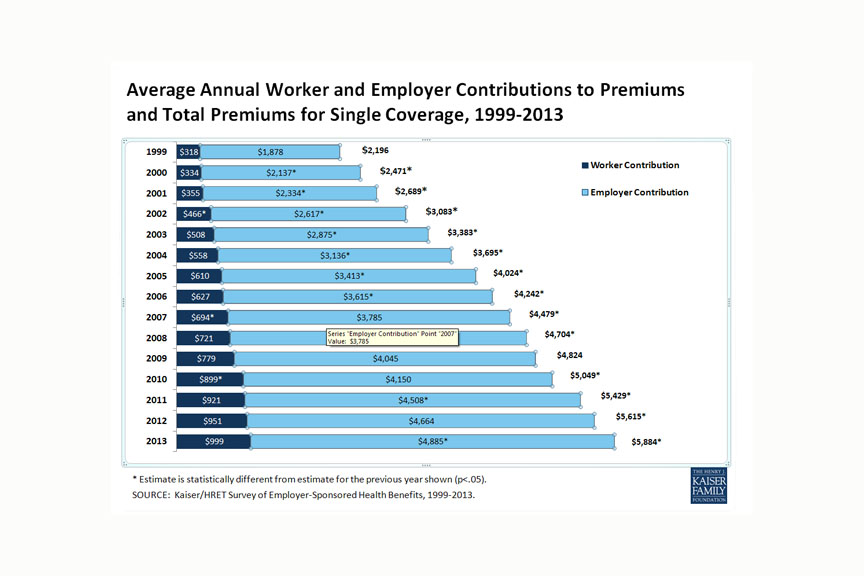

On average, it costs $5,884 in premiums to cover a single person through an employer-sponsored health plan this year, a 5 percent increase from last year, according to the survey.

The average cost for a family plan is $16,351, up 4 percent from 2012. That’s 80 percent higher than it was a decade ago.

The amount workers had to pay for that coverage didn’t change in a statistically significant way in the past year. This year, people pay an average of $999 for individual coverage and $4,565 for a family. On average, workers paid 18 percent of the premiums for single coverage, and 29 percent for family coverage, which the report said was relatively unchanged for the past decade.

But premiums are only a part of what people pay for health care. More than three-quarters of workers have plans with deductibles that require them to spend a certain amount of money before most services are reimbursed by the plan. This year, those deductibles averaged $1,135 for a single person, up more than 54 percent since 2008.

And Drew Altman, the Kaiser Family Foundation’s president and CEO,said the increased out-of-pocket costs consumers face are an important counterpoint to what he described as a year of “very moderate” premium increases.

“That’s not necessarily the public’s perception of what’s going on, because they don’t just pay their share of the premium, they pay other forms of cost-sharing, including especially their deductibles,” Altman said.

Size matters

This year, 57 percent of firms offer health insurance to at least some of their workers, according to the survey. That’s down from 61 percent last year, but the report noted that the change is not statistically significant.

Also unchanged: the differences between large and small companies.

Among companies with 50 or more workers, 93 percent offer insurance to at least some workers this year. (It’s even higher among those with 200 or more workers: 99 percent.)

As part of the federal health reform law, employers with 50 or more workers will be required to offer insurance or pay a penalty, although the Obama administration pushed back the “employer mandate” to 2015, rather than have it take effect next year as originally planned.

Among the smallest employers included in the survey, those with three to nine workers, only 45 percent offered insurance.

What will small businesses do?

Advocates for health reform have expressed hope that the law would help small businesses provide coverage. But some experts are skeptical that small companies that don’t offer coverage now will begin doing so.

Some small employers will be eligible for tax credits if they buy insurance through Access Health CT, the state’s health insurance exchange, a marketplace for buying coverage created by the health reform law.

But Brian Driscoll, chief operations officer at Ovation Benefits in Farmington, said the salary limits required to qualify for the tax credits are relatively low for the Northeast, making many companies ineligible. Firms can only get the tax credits if their average annual wages are below $50,000 and if they pay at least half of employees’ insurance premiums.

“There’s not a lot of employers that have qualified for that,” said Driscoll, a board member of the Connecticut Association of Health Underwriters.

Instead, Driscoll expects that some small employers will “take a hard look” at whether to continue providing coverage and possibly eliminate their health plans, allowing workers to buy coverage on their own through Access Health.

Among his company’s small-group clients — those that cover between two and 25 people — Driscoll expects about 10 percent will stop offering insurance.

Some employers are looking forward to the chance to stop providing coverage, Driscoll said, while others want to offer plans but are struggling with the increasing costs, having already raised deductibles to high levels.

People who buy coverage on their own through the exchange could qualify for federal subsidies to discount the premiums, if their incomes are low enough. Driscoll said some employers that drop coverage might boost workers’ pay to offset the lost benefits, but he noted that doing so could reduce the levels of subsidies employees could receive.

Your health, their business

Among larger companies with more than 50 employees, Driscoll expects there to be little move toward dropping coverage.

But some might be considering different ways to offer coverage. According to the Kaiser survey, 29 percent of firms with 5,000 or more employees said they were considering providing health benefits through a privately operated exchange in the future. In those cases, companies could give workers a set amount of money and let them choose from a variety of plans, meaning the employee would get more choice, but also more potential financial responsibility.

And even among companies that don’t make dramatic changes in whether to offer coverage or not, Barry Schilmeister, a principal with the consulting firm Mercer, said workers are likely to see another change: a growing focus on wellness programs aimed at improving employees’ health.

It’s being driven in part by a provision of the health reform law that taxes high-cost health plans, commonly referred to as the “Cadillac tax.” It takes effect in 2018, and will require employers to pay a 40 percent tax on health plan costs above $10,200 for an individual plan and $27,500 for family coverage.

The tax calculation is based on the total cost of the coverage, regardless of whether the company or the employee pays it. So simply shifting the costs to the workers, as many companies have done in the past, won’t help an employer avoid the tax.

Schilmeister said the impending tax on high-cost plans has led companies, particularly larger employers, to take a more long-term approach to reining in costs.

“This excise tax, to me, is really the back door incentive for cost-control, and I think you will see design changes that slowly are designed to bring the total cost of the programs down,” he said.

Those changes are likely to include increased cost-sharing, more lower-cost plan options, using narrower networks of health providers, and a greater emphasis on healthy behaviors, he added.

According to the Kaiser survey, the vast majority of employers offer at least one type of wellness program, although it defined those programs broadly, including biometric screening, smoking cessation programs, flu shots, wellness newsletters, gym membership discounts and personal health coaching. Fewer provide financial incentives to participate in wellness programs — just over a third of companies with 200 or more workers, and 8 percent of smaller firms.

“I think the watchword here for employees is you’re not only going to be more responsible for the cost of programs, but you’re going to be a lot more directly responsible for staying healthy and engaging in healthy behavior,” Schilmeister said.

“Employers who five years ago wouldn’t have thought to make the premium that you pay for your plan dependent on you getting your cholesterol screening or maintaining a certain [body-mass index], that’s on the table all the time now,” he said.

“Pretty soon it’s going to be the exception, where you’re working for a company that doesn’t have something like that, I would say.”