Conventional wisdom is that the total price charged by the state and its local governments in Connecticut is one of the most burdensome in the country. A common measure upon which this conclusion is based is the total amount we residents pay in state and local taxes, relative to our aggregate personal income, i.e., our capacity to pay. On this basis, the Tax Foundation tells us that Connecticut ranks either first or second highest in the nation, depending on which of two analytic models it uses.

However, taxes are not the only price paid to governments.

Residents also pay a number of fees and other charges, separate and distinct from taxes. David Osborne and Peter Hutchinson, in their landmark book, The Price of Government (2004), accordingly base their analysis on “the sum of all taxes, fees, and surcharges collected directly by a given locality, state, or nation” with respect to “that jurisdiction’s total economic resources [measured by total personal income].”

On the Osborne-Hutchinson measure, Connecticut’s price of government is not the highest. To the contrary, in FY 2002 Connecticut ranked fourth lowest in the country, behind only New Hampshire, New Jersey, and Tennessee. In FY 2007, according to an analysis by the New England Public Policy Center at the Federal Reserve Bank of Boston, Connecticut ranked third lowest. And as late as FY 2015, Connecticut ranked ninth lowest – in the lowest fifth – along with Georgia, Florida, Texas, Arizona, Tennessee, and New Hampshire, all states frequently cited as models for Connecticut to follow.

Why the disparate conclusions?

All three models referred to – the two developed by the Tax Foundation and the one defined by Osborne and Hutchinson – use the same two data sources. All three employ the total “personal income” in a state, reported by the U.S. Bureau of Economic Analysis, as a measure of economic resources. And all three cite data about state and local revenue from the U.S. Census Bureau, which sums the subcategories of “Taxes” and “Charges and miscellaneous general revenue” to arrive at all “General revenue from own sources” paid to state and local governments in a state. [The latter, generally referred to as “own source general revenue,” excludes revenue coming to a state from the federal government.]

However, the Tax Foundation analysts focus solely on the Census Bureau’s “Taxes” data subset. They fail to recognize Connecticut’s low use of fees and charges for the use of airports, state parks, school lunches, highways, state hospitals, sewer usage, etc.

Ignoring the contribution that non-tax sources make to the general state/local “own source revenue” can greatly alter a state’s ranking on a revenue-raising scale. A state with low fees and surcharges will rank higher if those fees and surcharges are not counted, and, vice versa, a state with high fees and surcharges will rank lower if they are not counted.

This distortion especially affects Connecticut’s ranking. Among all 50 states and the District of Columbia, Connecticut’s share of total state/local “own source revenue” which is derived from non-tax charges is the LOWEST in the nation. In FY 2015, the average state/local jurisdiction collected 31 percent of its “own source revenue” from fees and other charges, not taxes, while Connecticut collected only 16 percent of its “own source revenue” from fees and other charges.

In contrast, at the other end of the spectrum, Alaska collected about 61 percent of its total “own source revenue” from fees and other charges, and South Carolina, Wyoming and Alabama collected about 45 percent of their total revenue from these non-tax sources.

Measuring a state’s revenue solely on the basis of taxes drives the misperception that Connecticut local/state governments are collectively taking a higher-than-average share of economic resources from their residents in order to fund government services.

The Tax Foundation’s two widely cited models are flawed.

The Tax Foundation counts only taxes in both of its models.

In the latest version of its report – “State-Local Tax Burden Rankings, FY 2012,” published in 2016 – the Tax Foundation concluded that taxes on Connecticut residents, as a share of total state personal income, ranked second highest in the country. And its annual report on “Tax Freedom Day®” regularly reports that tax freedom day in Connecticut is among the latest in the country.

So it is no wonder that the Hartford Courant and the Connecticut Business and Industry Association repeat the common wisdom that Connecticut has “one of the . . . highest tax burdens.” Or that one gubernatorial candidate cites the Tax Foundation’s conclusion that “Tax Freedom Day®” came latest in Connecticut (in FY 2017), as proof that the state “has the highest total tax burden in the nation.”

By focusing solely on taxes, the Tax Foundation methodology fails to recognize Connecticut’s low use of fees and surcharges.

Moreover, Tax Foundation analysts compound their tax-centric analysis by modifying the Census Bureau data on “Taxes” to include taxes levied by other states on Connecticut residents as part of Connecticut’s tax burden. Revenue from these out-of-state taxes are not received by Connecticut governments. And these taxes are beyond the reach of Connecticut policymakers, so their inclusion distorts state-to-state comparisons. No matter what Connecticut government does, its actions won’t affect any out-of-state taxes, which include the following:

- Personal income taxes paid to New York and/or New York City (or other states), by Connecticut residents who work in those locations,

- Property taxes on vacation or second homes located in other states,

- Sales taxes and amusement taxes paid to other states due to vacation travel (hotel bills, car rental fees, entertainment, etc.)

- Severance taxes on oil, natural gas and coal production in states such as Louisiana, Wyoming and Alaska, and incorporated into energy bills paid by Connecticut residents.

According to the Tax Foundation, only 70 percent of the per capita tax burden on Connecticut residents is based on taxes levied by Connecticut state/local governments.[2] The magnitude of the distortion, in actual dollars, is the largest in the country.

Furthermore, if those taxes attributed to other states by the Tax Foundation are excluded from calculations, Connecticut’s rank among all states and D.C. in the Tax Foundation’s “State/Local Tax Burden” model – which looks at taxes alone – drops from second highest to 15th highest in FY 2014.

Additional flaws in the Tax Foundation’s second model: “Tax Freedom Day®”

Several other methodological problems underlie the Tax Foundation’s assertions that Connecticut had the latest “Tax Freedom Day®” in the nation in 2017, and the third latest “Tax Freedom Day®” in 2018 (May 3).

The Tax Foundation’s calculation of TFD® is infected with the same methodological flaw discussed above: the basis for each state’s share of the overall ranking includes taxes levied by other states – which in Connecticut is 30 percent of the total state/local tax burden.

Moreover, the calculation includes taxes levied by the national government (including Social Security and Medicare taxes) as well as taxes levied by each state’s state/local governments. On average, 65 percent of the taxes which contribute to the determination of TFD® are national. So if Connecticut were an average state, only 38 of the 109 days until April 19 (the average TFD for 2018) could be attributed to the state and local tax burden

But Connecticut is not an average state: its residents have higher incomes than most other states, so its residents pay more than the average national share of the aggregate tax burden. Because the federal income tax system is progressive, states with greater numbers of high-income residents pay more federal taxes than states with fewer high-income residents.

Of course, there is no question that differing tax policies in the states also affect the date of TFD, although the opaque nature of the Tax Foundation’s calculations makes it difficult to sort out exactly how much state tax policy influences the outcome. But the fact that Connecticut’s per capita income in 2014, $39,373, was 36 percent higher than the U.S. average of $28,889 certainly is an indication that higher incomes in Connecticut have a major impact on the lateness of TFD.

As the Tax Foundation itself notes, the “progressivity of the federal tax system” means that, in part, “states with higher incomes . . . celebrate TFD later.” So tax freedom day® comes later in Connecticut (May 3 in 2018) mainly because of the affluence of the state, combined with the progressive federal tax structure.

Price of government (POG) model

Unlike the data used by the Tax Foundation models, the Osborne-Hutchinson model uses the total “own source general revenue” data reported by the Census Bureau, including both taxes and other charges – with no adjustment or modification.

The Osborne/Hutchinson metric has been adopted and used by non-partisan, non-ideological policy analysts since it was first elaborated. The New England Public Policy Center at the Federal Reserve Bank of Boston replicated it in 2010, and it is the basis of the annual rankings of states through FY 2014 by the Minnesota Department of Revenue, which were recently updated for FY 2015 by the North Star Policy Institute.

All analysts using this model have found that the price of government in Connecticut is consistently one of the lowest in the country – ranging from third lowest to ninth lowest.

Specifically, here are rankings of Connecticut based on the POG over a period of years:

| Fiscal Year | Source | Cents per Dollar of Aggregate Personal income in Connecticut | Cents per Dollar of Aggregate Personal Income – National Average | Percent Connecticut is Below the National Average | National Rank each year (# from the bottom) |

| 2002 | Osborne and Hutchinson, The Price of Government | 12.8 | 14.9 | 14.1% | 4 |

| 2007 | NEPPC at the Federal Reserve Bank of Boston | 13.7 | 16.1 | 14.9% | 3 |

| 2010 | Minnesota Dept of Revenue | 13.7 | 15.6 | 12.2% | 8 |

| 2014 | Minnesota Dept of Revenue | 13.5 | 15.3 | 11.8% | 7 |

| 2015 | North Star Policy Institute | 13.1 | 14.9 | 12.1% | 9 |

In all of the years cited, Connecticut’s “own source revenue” as a share of personal income was far below the national average. For FY 2015, Connecticut’s price of government, at 13.1 percent, was 1.8 percentage points below the national average of 14.9 percent.

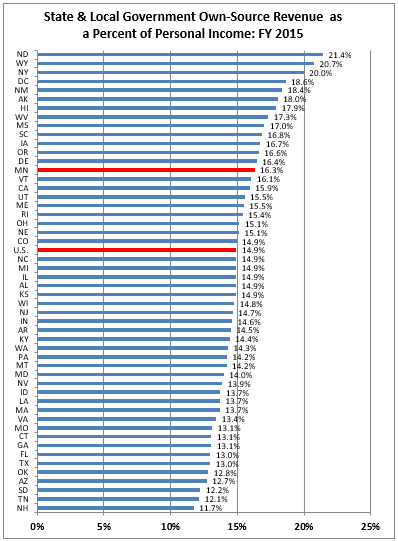

The complete chart for FY 2015, based on the Osborne-Hutchinson model, is printed below:[8]

Source: North Star Policy Institute. Used with permission.

And although preliminary Census Bureau data for FY 2016 – available on Sept. 7, 2018 – has not yet been fully analyzed, those data indicate that the share taken by Connecticut state and local governments for that year dropped to 12.6 percent. Its rank is not yet available.

Flawed models produce deceptive results

Counting all “own source general revenue,” the share of the economic resources of Connecticut that is paid by its residents to state/local government for the services those governments provide, ranks Connecticut among the lowest in the nation.

Other conclusions produced by flawed models, based on only a portion of in-state revenue – taxes – and including non-Connecticut taxes, should be disregarded. Those models deceive residents into thinking that a situation is worse than it really is – the very opposite of a Potemkin Village.

Bill Cibes is Chancellor Emeritus of the Connecticut State University System; was formerly Secretary of the Office of Policy and Management under Gov. Lowell P. Weicker; and recently retired as a board member of the Connecticut News Project, publisher of the Connecticut Mirror and CTViewpoints.