Student loan debt relief changed my life. I didn’t get relief because I was smart, kind or even savvy. I got it because I was lucky. I paid my way through undergrad with scholarships, grants and a few loans. My graduate school debt burden was an entirely different story and made it hard for me to meet basic expenses like rent and food. A colleague’s family understood this and included me in Jubilee gifts (debt forgiveness based on Biblical text) they were making to a number of people. This gift — a check for $20,000 written directly to my student loan servicer — changed my life, and made me understand how important direct relief can be.

Connecticut graduates have more debt than those in any other part of the country and borrowers of color and first-generation college students are most deeply impacted by the student debt crisis. Nationwide, black students borrow more than other students for the same degrees, are more likely to drop out without receiving a degree and owe $7,400 more than their white peers at graduation. The student debt crisis impacts middle-class minorities the most.

Four years after graduation, the racial debt gap more than triples with blacks owing nearly $53,000 in student loan debt — twice the debt of their white counterparts. Black students pay higher interest rates, borrow more for graduate school and earn less than their white counterparts. These disparities exist even after controlling for family income and wealth.

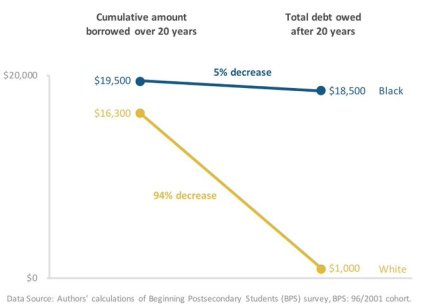

Instead of propelling families and lives forward, the $1.5 trillion in student loan debt we carry is actively holding us back. College attendance and graduation is no longer a certain path to the middle class. In fact, 20 years after graduation, a typical white borrower sees a 94% decrease in their student loan debt while a black borrower’s debt has decreased only 5%. (see chart) Again, systemic inequities – interest rates, loan type, wages, and generational wealth influence the outcome.

Borrowers continue to buy into the idea that college attendance equals increased earning power. In fact, family economic advancement is at the very root of the decision for many to attend. But students, and, particularly students of color, are being sold a bill of goods. When earning power is too low and debt burdens too high, students of color are restricted by their choice to attend college – not set free by it. We can not ignore the racial disparity of the debt burden.

Student loan debt relief leads to decreased overall debt as well as family wealth building, but debt relief must partnered with systemic change. We must fundamentally reconstruct the student loan system from the first time borrowers encounter potential student loans until their last payment of the loans. Universities and colleges must critically evaluate their financial aid practices, high schools and families must educate college applicants on student debt assessment as part of the college search process, and we must change this unjust and inequitable system.

Anne Watkins is the founder of the Student Loan Fund in New Haven.

Once again, student debt needs to be solved using the “Cause vs Effect Model”. The root cause of this problem is the excessively high cost of higher education. Not the cost of borrowing. Fix what is driving the cost of higher education…fix the problem!

Why are so many trying to forgive student loans. They signed it they own it. I signed my mortgage right before the 2008 crash. No one is offering me any help on my mortgage. If you sign for a loan own it

You have hit upon the problem. People think that others will always bail out their mistakes. There’s always a Bernie or Liz waiting to offer free stuff paid by hard working tax mules.

You haven’t mentioned the root cause of the problem. How an analysis of value versus cost. I was accepted but could not afford the university of my choice. I instead chose to save money and do the first 2 years at a community college and live at home. I saved and paid my own way through my 4-year university, working a part time job all year long. Prior to going to grad school, I made sure my employer offered tuition assistance. They paid for 1/2 my JD, I borrowed a 1/3 of the rest. In the end, I am debt free and got a terminal degree by working hard and balancing the costs with the benefits. I look back and realize I missed nothing at that overly expensive first choice, and am glad I’ve had the experiences I’ve had. Time for people to be responsible for their decisions, I’m not impressed with excuses and will not be voting for anyone talking about tuition forgiveness or tuition at taxpayer expense.