Before the pandemic hit, Connecticut’s economy was in sad shape. During the 10 years leading up to 2020 the U.S. economy grew by 19% but Connecticut’s shrank by .5%. Once COVID-19 is finally behind us, we’ll need to drive up demand for jobs, raise state revenue and make investments favorable for businesses.

But here are problems which leaders need to solve: Economic shifts have made Connecticut’s revenue system dysfunctional. Wage stagnation and jobs lost to other states or countries are cutting revenue. Consumer buying power is no higher today than it was in 1980. Even though per capita income is higher than all other states, spending is too limited to raise demand for jobs.

Why does our growth lag behind other states? Could it be the desire for professional couples to find dual incomes in larger metropolitan areas such as New York or Boston? Maybe. Twice the number of Connecticut residents have found jobs out of state than out-of-state residents have found here. That means less income subject to Connecticut income tax.

Or could it be due to a change in how business is conducted? “Over the last dozen years, American’s largest firms taken as a whole haven’t invested more than 1-2 percent of their total assets per year into the real economy-real jobs, real goods, real services….” Instead, profits are being made through financial engineering, i.e. debt leveraged buyouts, mergers, acquisitions, job cuts, asset sales, tax avoidance schemes and stock buybacks. Profits which used to drive wage increases and business expansion are being made by cutting these very items, thereby shrinking the tax base.

The problem extends to all four elements of Connecticut’s Gross State Product;

- Consumer spending –buying power has not grown since 1980

- State and local government spending on wages and salaries is fifth lowest of all states

- Net state exports are negative

- Capital investment has been at 1.6%, well below the national average of 2.7% of personal income.

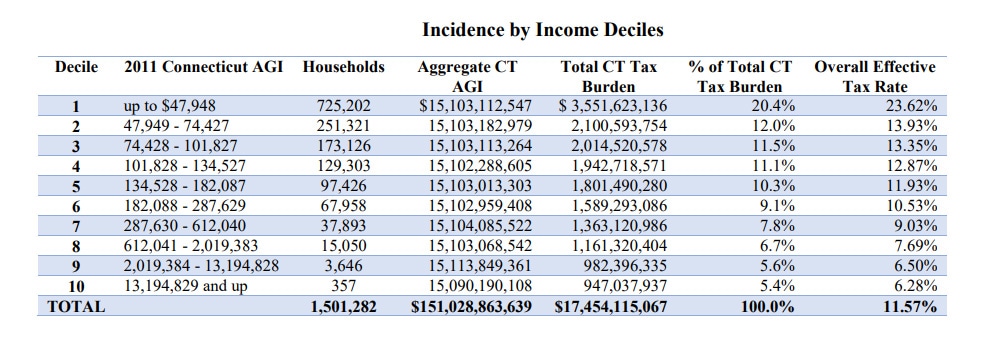

Take a fresh look a Department of Revenue Service’s Tax Incidence Study done in December 2014, [see the table on page 8] in light of prolonged wage stagnation and pandemic job losses. It shows that families in the lowest 10% in income paid nearly 24% of their income in state and local taxes. How can these families and others burdened with disproportionate state and local tax rates possibly afford the consumer spending necessary to keep the state’s economy from shrinking?

Connecticut has the highest income of all states but it’s doing little for the state’s economy. That’s because most of it is just accumulating in the investment portfolios of residents high in the 1%.

According to Adair Turner, Chairman of Institute For New Economic Thinking: “A mere 15% of all financial flows now go into projects in the real economy. The rest simply stays inside the financial system, enriching financiers, corporate titans, and the wealthiest faction…” This view explains why capital investment has been so marginal.

While the economic landscape shifts, an outdated revenue system is pulling the rug from under the state’s fiscal feet. Dozens of proposals have been offered as revenue dwindled, but nearly all have been sidelined, presumably because they require wealthier residents to pay a more proportionate share of state and local taxes.

We need a revenue system that works for the economy we have now. As a starting point, legislators should work up a plan to rebalance state and local tax burdens fairly. That would boost consumer spending and drive up demand. Knowing this has to be paid for, some very high income residents have offered to raise their taxes. Let’s not fail to act on their good intentions.

William Buhler lives in Cromwell.