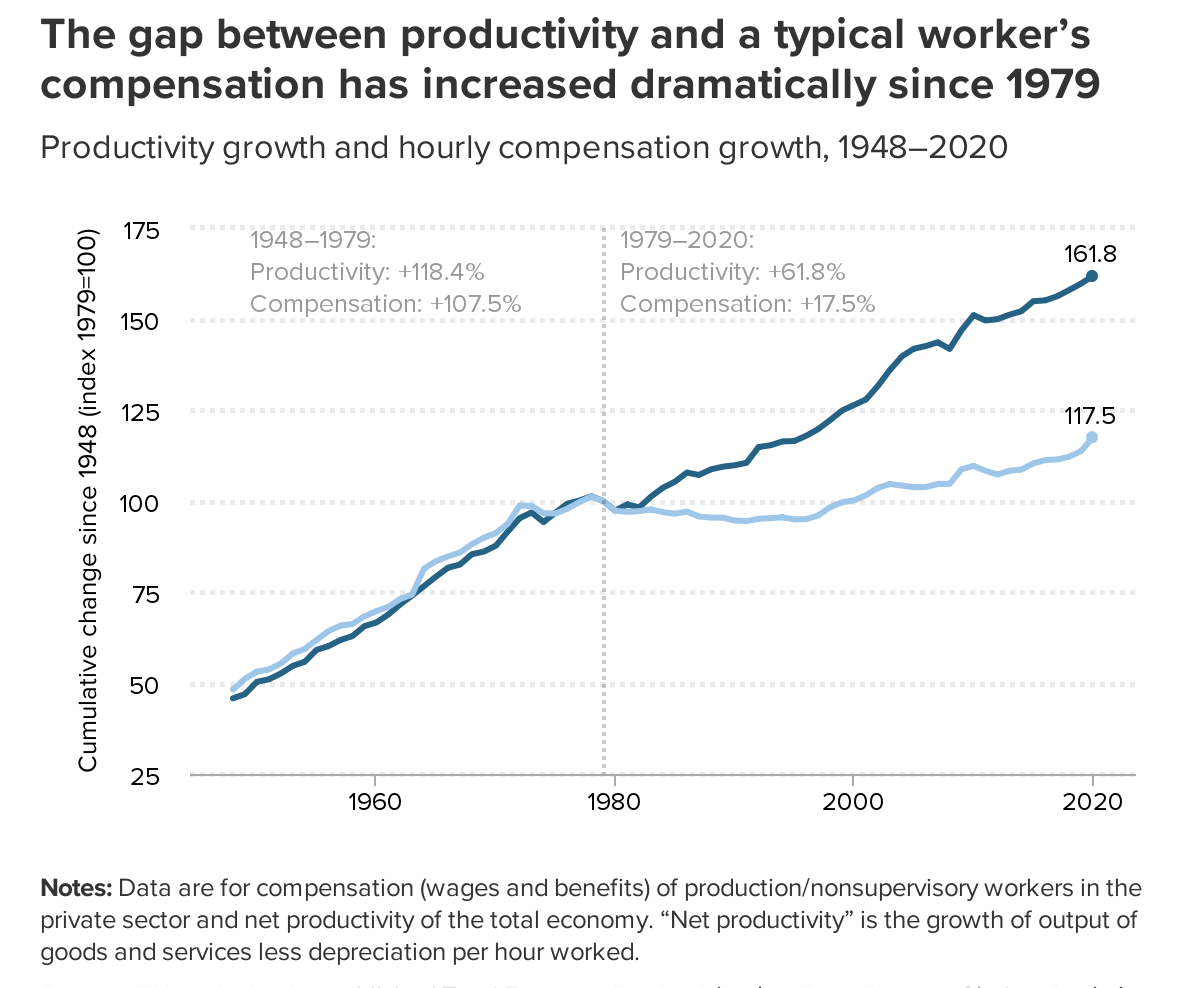

Should everyone share the rewards in a growing economy? Connecticut policymakers guided by that belief changed course in 1979 and began to dismantle protections that ensured worker’s pay would grow with company productivity. Since then the gap between company productivity and worker’s pay widened, eventually undermining Connecticut’s robust economy.

So far that economy has not returned to the robust level it sustained in the decades prior to 1991, and state revenue growth remains at less than half of what it used to be. While there have been numerous changes to the state’s tax code, the combined tax burden still falls most heavily on those least able to pay. A recovery for Connecticut’s economy should begin with an equitable rebalancing of state and local taxes.

State revenue began to fall in 1989 and by 1991 tax changes were necessary to offset a large budget deficit. Those tax changes — the best known of which was the passage of the Connecticut’s first income tax — had a highly positive effect on the economy of Fairfield County; during the 10 years after their passage they saw a 66% increase in employed residents along with a boom in the financial services industry. Unfortunately no such growth occurred elsewhere in Connecticut. During the 90’s decade there was a statewide 3% drop in the number of people employed.

By 2013 the pay and productivity gap in Connecticut grew to where those in the 1% were capturing 80% of all income growth. The state’s economy contracted by .5% during this decade even though the U.S. economy expanded by 19%. This should have been cause for great concern.

Income gains captured by the well-off are often saved as personal investments which have no stimulative impact on the real economy. There’s no need for entrepreneurs to build factories and hire workers to make a profit because in today’s economy investments in the stock market yield faster returns.

Income gains of wage earners are often spent, creating waves of economic expansion as money changes hands. That spending is the main source of economic growth, but due to stagnating wages, consumer spending power is no higher today than it was in 1980.

Adding to the problem of lagging consumer spending power, Connecticut’s regressive tax code burdens families in the lowest 10% with combined taxes that consume nearly 24% of their income. As of 2014 such families comprised nearly half the households in the state. Those in the top 10% pay less than 7%. The state tax code itself is an engine of inequality which further reduces consumer spending power.

In the 50’s, 60’s, 70’s and through most of the 80’s Connecticut had a robust economy which rewarded residents with a rising standard of living. State revenue grew at an average rate over 10% per year and surplus revenue was often carried forward. Most people expected good times to continue, but those carefree days began to slip away as the decade of the 80’s came to an end.

All was not well on January 9, 1991 as newly elected Gov. Lowell Weicker Jr. was sworn in. The real estate bubble had burst and thousands of jobs were disappearing as the banking and defense industries contracted. There was a huge budget deficit and forceful action was necessary to raise new revenue. In the midst of this turmoil the new Governor from Greenwich would push through an array of tax changes that resolved the budget shortfall but did little to restrain the growing income gap.

As Governor Weicker looked for revenue options, he noted that Connecticut’s 8% sales tax was already the highest in the nation, so he turned elsewhere. After consulting with the Office of Policy and Management he saw no way to avoid the necessity of an income tax. He envisioned it as a broad based 6% tax on earned income with some offsetting corporate and sales tax cuts. Taxes on interest, dividends and income gains from the sale of stocks, bonds and real estate would be lowered to the rate for earned income.

The existing tax on capital gains was 7% and the tax on interest and dividends was at 14% for those with high incomes. So at the first public hearing New Haven State Rep. Irving Stolberg asked colleagues to admit the tax proposal wasn’t progressive enough and benefitted those in the highest brackets. Residents earning under $40,000 would bear the brunt of the tax, he asserted, when income, sales and property taxes were combined.

After a June 30 vote stuck down the Governor’s proposal, infighting and wrangling stretched into the hot summer of 1991. Continuing resolutions allowed the state government to stay open after the close of the fiscal year. Negotiations continued seven days a week and were described as “the closest thing to combat…” State Sen. William DiBella worked on deal making and got Sens. William Nickerson from Greenwich and Lawrence Bettencourt from Waterford to support a bill that would include reductions in capital gains, interest and dividend taxes, tax cuts they believed would benefit many of their constituents. On Friday, August 23, the final version of Public Act 91-3 was passed with the thinnest of margins, a tie breaking vote by Lt. Gov. Eunice Groark.

The final version of Public Act 91-3 included a flat 4.5% income tax which fell heaviest on middle and upper middle income families. Offsetting the income tax were substantial tax cuts: Sales taxes were reduced from 8 to 6%. Capital Gains taxes were dropped from 7 to 4.5%. Interest and Dividend taxes, formerly at 14% for those with high incomes, were reduced to 4.5%, and there was also a 12% cut in corporate taxes. The bill benefitted those at the top, particularly those with significant investment income and owners of capital.

Executives and hedge fund managers living in Fairfield County but employed in New York were paying over 7% in New York income taxes and saw an opportunity to profit with the new tax system; PA 91-3 incentivized them to relocate their businesses to where they lived and pay only 4.5%.

In an unintended display of asymmetry, PA 91-3 was also held to “benefit” those at the bottom due to the sales tax cut and the exclusion of the first $24,000 of income for married couples, tax cuts which applied to all income levels.

Death threats and protests ensued after the passage of the bill. Bettencourt was run off the road by someone driving a pickup truck. One house was struck by gunfire. Legislators were encouraged to remove identifying license plates.

Former Sen. Tom Scott organized a “Taxpayers Committee Rally” at the Capitol to revoke the bill. It drew 40,000 residents, the largest protest at the Capitol in state history. The Governor came out to address the mass and commented that many of the protesters probably did not earn much over the amount of income excluded from the tax. Nevertheless, repeal efforts continued for three days of public hearings in late November. The House voted for repeal but not in sufficient numbers to override the veto of the unwavering Governor.

Having reached an impasse, the exhausted legislators sensed it was fruitless to continue fighting and voted 80 to 68 to go home. The passage of Public Act 91-3 established a new tax structure, one which brought in new revenue and would redefine the winners and losers in the years ahead.

William Buhler lives in Cromwell.