This story has been updated.

Connecticut’s small businesses and nonprofit organizations could see lower health insurance costs under a proposed bill that would allow trade associations to offer large group health plans to their members.

But patient advocates say they’re concerned about language in the legislation, House Bill 6710, that could allow plans to charge higher rates to companies employing people who get sick or injured.

More than three dozen legislators, trade group representatives, patient advocates and individuals submitted testimony for a public hearing on the bill slated for Tuesday afternoon. Ahead of that hearing, a bipartisan group of lawmakers held a press conference calling for its adoption.

“This coalition here is forming a new option of plans for small businesses, plans that are unique and affordable and that will help create more competition in the market,” said Rep. Kerry Wood, D-Rocky Hill, who co-chairs the Insurance and Real Estate Committee.

“We need to stand behind those campaign promises and pass this bill that will expand and make health insurance more affordable for small businesses across the state,” said Rep. Cara Pavalock-D’Amato, R-Bristol.

Association health plans are currently available to businesses in roughly a dozen states, but there is some uncertainty over regulatory gaps between state and federal law governing them.

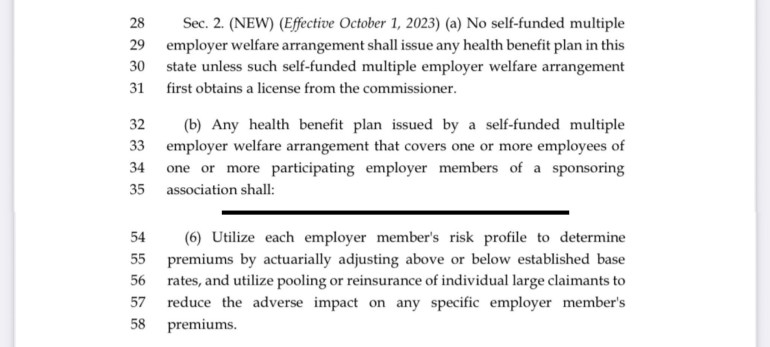

Connecticut’s H.B. 6710 would allow established trade associations that meet certain membership requirements to purchase fully funded health plans from insurance companies as a group, or they could offer what are known as “self-funded” insurance plans, where a large employer — in this case the trade group — pays claims directly. (In Connecticut, about 76% of privately insured people are covered by self-funded plans, which are regulated by the federal Labor Department rather than the state Department of Insurance.)

Small organizations currently have to shop for their own fully funded insurance plans in the marketplace each year. Many who want to offer benefits to their employees say steep rate hikes have made that nearly untenable. And the recent departure of ConnectiCare from the state’s fully funded health insurance marketplace has raised further concerns about health insurance accessibility and affordability.

Bruce Adams, president of the Credit Union League of Connecticut, which counts about 60 member organizations, said association health plans would open up more affordable options for many organizations.

“If our 60 members all signed on to one plan, we would have a couple thousand people in our group, so clearly we could obtain health insurance at a cheaper rate,” Adams said. “That helps level the playing field among the financial services industry, because banks are bigger than credit unions, and it allows for the small business in Connecticut to thrive.”

Still, advocacy groups such as the American Cancer Society, the Leukemia & Lymphoma Society and Health Equity Solutions opposed the legislation. In testimony before the General Assembly’s Insurance and Real Estate Committee, they expressed concerns that the plans would favor healthy people.

Ernie Davis of LLS highlighted a section of the bill, Sec. 2(b)(6), that he argued would allow self-funded plans to “adjust the premiums charged to any single member-employer within the association based on that employer’s claims experience.”

In other words, Davis wrote, if a company has an employee who is diagnosed with blood cancer and needs treatment, the following year the health plan could raise that company’s premiums — potentially rendering the AHP an unaffordable option, “meaning they will lose the benefit of joining the association in the first place,” Davis wrote.

He likened AHPs to “health sharing ministries,” nonprofit religious organizations that pool their members’ contributions with the intent of paying out medical bills, though there is often no guarantee of coverage.

“I appreciate that folks are out there looking for new ways to provide affordable health benefits,” said State Health Care Advocate Ted Doolittle. “But as it’s currently constituted, I do have concerns.”

Doolittle said if AHPs wind up favoring companies with healthier employees, that could raise the risk pool for people who seek insurance on the public exchange. “That’s bad for Connecticut, because if all the healthy small businesses in Connecticut go into an AHP and all the unhealthy ones go on the exchange, then premiums go up.”

But proponents pointed out that unlike the self-funded plans currently used by many large employers, which are regulated at the federal level, association health plans would be subject to state regulation under the bill.

“All of these issues can be addressed in statute. The state has the ability to design this however they want,” said Wyatt Bosworth, a lobbyist with the Connecticut Business and Industry Association, which supports the bill.

Companies with healthier employees might pay lower rates in AHPs, “but the question is what will the swing be,” Bosworth said. “The state has the power to say you can’t vary rates by more than some percentage.”

Rev. Josh Pawelek, who leads the Unitarian Universalist Society: East in Manchester, was in the Legislative Office Building cafeteria Tuesday morning, waiting to testify at another public hearing. He said he wasn’t aware of the AHP legislation but he shared some of the concerns of those who opposed it.

UUS:E can’t afford top-of-the-line insurance, but its current plan has covered the costs of major illnesses, Pawelek said. If a plan were to charge more based on his organization’s health experience, “I think that’s a nonstarter for us,” he said.

Doolittle, the state Health Care Advocate, said making health insurance affordable is important, but it takes more than just a new health plan option.

“I want health insurers to come up with innovative plans that achieve affordability by tackling the internationally abnormal medical and drug prices that are the cause of unaffordable health premiums and out-of-pocket costs,” Doolittle said.

“Making health insurance cheaper for healthy people and more expensive for sicker people is a Band-Aid that ignores the real source of the American health spending crisis,” he said.

Clarification

About 76% of privately insured people are covered by self-funded plans, according to the state Insurance Department. A previous version of this story, citing incorrect information from the Office of the Healthcare Advocates website, said about half were covered by self-funded plans.