Donna Denby used to sell antique buttons — most of them made before 1930, some adorned with early Disney characters, and no two alike — but in 2020, the pandemic effectively shut down her business.

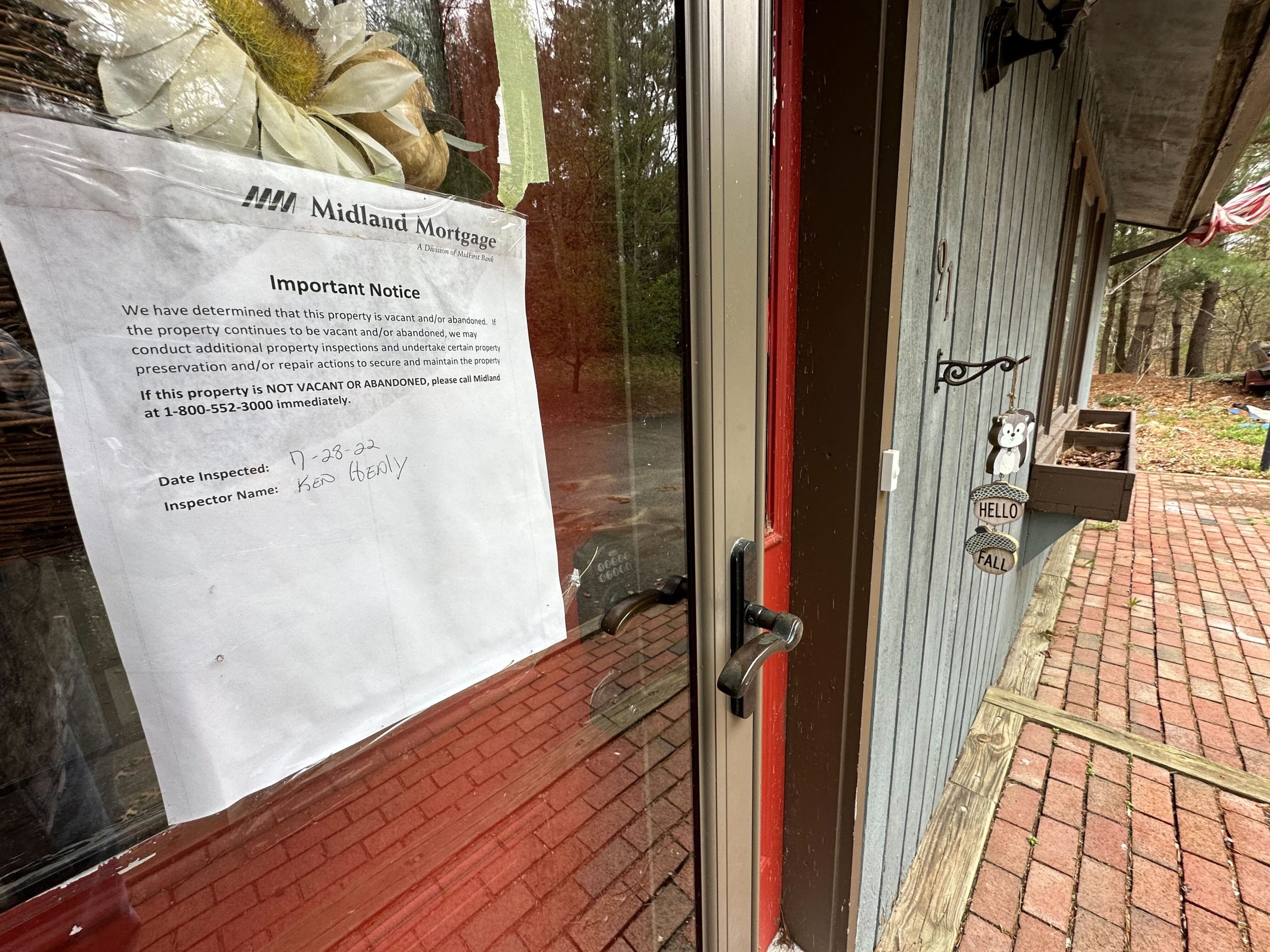

She thought she could wait it out and dipped into her savings to cover her living expenses. But as the months ticked by, she fell further behind on the mortgage for her Monroe house. She was shielded from foreclosure by pandemic-era protections, but she feared what would happen when those expired.

“I used all my savings just to live, basically,” Denby said. “I wasn’t used to that.”

During the pandemic, Congress created the Homeowner Assistance Fund through the American Rescue Plan to offer financial aid to homeowners who have fallen behind on payments. The federal government also allowed up to 18 months of forbearance, or temporary pauses on mortgage payments.

The ARPA money was disbursed to states to establish programs for homeowners. Connecticut’s has seen faster spending in recent months after a slow start.

In part because of aid from foreclosure prevention programs, the number of finalized foreclosures in Connecticut is down significantly compared to pre-pandemic levels. Still, foreclosure filings — an early stage in the foreclosure process — are up compared to last year, primarily among a population that likely doesn’t qualify for the pandemic aid, housing experts said.

Connecticut received $123 million in federal ARPA money for MyHomeCT, the state’s program aimed at keeping people in their homes after financial losses during the pandemic. More than half of the money has either been spent or earmarked for ongoing payments.

About 3,000 households have received help, and the median amount of assistance is close to $21,000, according to the program data dashboard. The maximum allowed is $50,000.

Connecticut’s program allows either a one-time payment to cover bills owed or ongoing payments for people who can’t pay future bills. The money can be used for paying a mortgage, sewer liens, real estate taxes or condominium fees, among other debts.

To qualify, applicants must have had a financial hardship because of COVID-19 and earn up to 150% of the area median income. For a New Haven family of four, that would be $168,900 annually.

Denby is one of the homeowners who was able to get assistance from MyHomeCT. She received about $50,000, the maximum allowable under the program, and got connected with the assistance through Bridgeport-based nonprofit Building Neighborhoods Together.

The Connecticut Housing Finance Authority, which manages MyHomeCT, has adapted its program in recent months to make the process quicker and more efficient. The state more than quadrupled the number of homeowners assisted and funds disbursed in the last three months of 2022, according to a report released earlier this month from the U.S. Department of the Treasury.

The authority has done outreach work with foreclosure mediators, mortgage servicers and tax authorities. It has also increased the number of staff working on the program, said Marcus Smith, director of research, marketing and outreach at the finance authority.

Compared to pre-pandemic levels, the number of finalized foreclosures in Connecticut is down so far this year, according to data from the finance authority. They’ve averaged about 36 per month since the start of 2022, compared to an average of 233 per month in 2019.

But recent months have seen an uptick in foreclosure filings, one of the early steps in the foreclosure process. Foreclosures in the first quarter of 2023 were up to 1,864 from 1,362 in the first quarter of 2022, a nearly 37% increase.

Experts say it’s not likely these numbers point to a housing crash anytime soon.

Many servicers are more willing to work with clients than they were in years past, said Adam Beattie, operations manager of the BlueHub SUN foreclosure relief program.

Zombie debt

Many of the people who are turning to the Connecticut Fair Housing Center for help dealing with a foreclosure filing are at risk of losing their home because of what’s called “zombie debt,” said Loraine Martinez Bellamy, an attorney at the center who focuses on foreclosures. Data doesn't make it immediately clear what portion of filings are zombie debt foreclosures, but attorneys are seeing more calls about foreclosures of this type.

Many homeowners took out second mortgages during the housing market bubble from about 2005 to 2006. When the market crashed in 2008, many didn’t make payments, and because the houses had low value, lenders stopped asking for the money.

Essentially, the price of the house wasn’t worth the cost of foreclosing.

But as the market picked up and houses became worth more in recent years, some lenders came after those loans again and filed foreclosures, Martinez Bellamy said. Homeowners had either forgotten about the debt or thought it had been canceled because they haven’t gotten any messages about it for more than a decade.

“It created an opportunity for these ‘zombies’ to wake up from the dead, and there’s been a lot of foreclosures started from these fly-by-night lenders,” Martinez Bellamy said.

The types of loans issued during that time aren’t used often anymore, said Patrick Gourley, an economics professor at the University of New Haven.

Gourley said homeowners who get a letter about foreclosure because of a loan that’s more than 10 years old should contact an attorney and remember that the letter doesn’t necessarily mean a foreclosure has been filed.

The center’s attorneys have been able to help several clients get the debt reduced or discharged on the “notion that if you don’t collect on a mortgage for 10 or 15 years, you lose the right to do so,” Martinez Bellamy said.

The center is also helping people get access to the MyHomeCT funds, although most who are facing foreclosure because of old loans aren’t eligible, she said.

MyHomeCT

After a slow start, Connecticut's foreclosure prevention program has gotten more staff, grown more efficient, and is getting money to people more quickly.

Connecticut was one of few states to implement an early pilot program for its foreclosure prevention program. It was then expanded into another phase, and the full program launched in May 2022.

The finance authority has until September 2025 to spend its funding.

Early phases saw slower spending because fewer loan servicers participated and the maximum assistance amounts were lower. The finance authority has done additional outreach to servicers and tax authorities to ensure they’re on board, Smith said.

They’ve also tried to make sure that homeowners can access the funding during the mandatory mediation portion of Connecticut’s foreclosure process, Smith said.

Review time has gotten quicker as the program increased staff to resolve a past backlog and the staff got more comfortable with the process. Reviews were typically finished in 19 days in March, Smith said.

“We continue to evaluate how the program is performing, learn from it and adapt,” Smith said in an email.

Delayed payments can result in more debt stacking up and more stress, Martinez Bellamy said.

“It does just complicate things because the number is a moving target,” she added.

Sometimes, issues arise if homeowners owe more than the $50,000 limit for MyHomeCT. They can pair that with other grants or with a payment from their own bank accounts, but some servicers won’t initially accept what appear to be “incomplete payments,” or payments from different sources that add up to the complete amount.

About 22% of applications so far have been denied. The most common reasons are that the application was incomplete, the homeowner needed more than the $50,000, there wasn’t a COVID hardship, or their incomes were too high, Smith said.

In the cases of homeowners who need more than $50,000, loss mitigation specialists work with the applicant and servicer to find a solution, often that a portion is paid by MyHomeCT and the rest is paid by the homeowner, Smith said.

Martinez Bellamy said she’s seen improvements in the program for her clients.

Denby’s experience with the program wasn’t as quick or smooth as others, she said. She first got her application finished in July, and the money wasn’t paid until December.

Building Neighborhoods Together helped her with the application, which was initially denied because of an issue with her lender. Carol Cruz, a housing counselor at BNT, helped advocate for Denby and get the issues sorted out.

“When she was denied, I had to make sure that I contacted the lender, and there was a lot of back and forth,” Cruz said. “And she wouldn't give up.”

After the back and forth, Denby will get to keep her home. Her favorite room is the sunroom, where she can see some of the animals that come to her yard.

“It’s a pretty, bright, cheery place, and all the birds come and eat up on the deck,” she said.

BlueHub SUN

Other programs have also found success at preventing foreclosures, including one nonprofit that helps people in several states, including Connecticut.

Trevor Johnie, a Waterbury resident who fell behind on his mortgage, got help through nonprofit BlueHub Capital. The group has a mortgage loan program that works with people going through foreclosure.

The program, called BlueHub SUN, refinances or buys homes in foreclosure to sell back to the original owners with a new mortgage. The new mortgage is more affordable to the owner, said Adam Beattie, operations manager of the foreclosure relief program.

People who participate agree to pay the new amount on time in the future, Beattie said. The program works across a few states, including Connecticut.

“It’s ideal for people who have kind of had a hardship, fell behind on the loan, but now have income and can afford a reasonable payment but just can’t get a work out with their servicer,” Beattie said.

Johnie, who moved to Connecticut from the Caribbean more than 30 years ago, started having problems paying his mortgage in 2017 after his older sister died. After traveling to be with her in her last days and staying to arrange the funeral, he was behind on payments. He struggled with work because of the depression he experienced after her death.

"She was the world to me,” Johnie said. “She took care of my girls. My sister had a big influence on my daughters. A big chunk of me is gone, losing my sister.”

Then, when the pandemic hit, he was still behind and lost work as a truck driver. He started working with BlueHub SUN to get his mortgage back down to a level he could afford.

He worried that he’d have to give up his home in a short sale and take very few belongings with him. But BlueHub bought his house and sold it back to him, he said.

“I was just praying,” Johnie said. “They [the former mortgage servicer] were sending me letters and giving me days to get out of the house. It was just a godsend.”

Now, he’ll be able to stay in his house. He’s getting ready for one of his older daughters to move to the United States with her kids, he said. They’ll probably stay with him for a while until they get on their feet in a new place.