In June of 2021 I advocated in these pages for towns to consider more closely the potential tax fairness of special districts under Connecticut law.

Such districts, properly deployed, could, I argued, work to level the incidences of property taxes within many towns, especially those towns where particular benefits inure principally to a limited part of the population, while the cost by is borne everyone through taxes.

I want to offer here further perspective of how special taxing districts in Connecticut currently work as part of my ongoing effort to tell the story of the modern Nutmeg State economy.

These special districts conspicuously cluster near natural attractions, such as the ocean and other bodies of water. Several towns host more than one district. Figure 1 maps out their locations and density.

From 2002 through 2022, Connecticut added 49 additional special districts, about a 13% increase. The number of special districts has nearly doubled since 1967.

The statutes provide for, in effect, four types of special districts. These include fire districts, utility districts (water and sewer), beach and lake associations, and improvement districts (condominium and other residential developments). The first two categories might be characterized as providing public services for public purposes. Beach and lake associations and improvement districts, however, unambiguously provide public service for private purposes.

More directly, these latter two types of special districts enable residents to receive benefits not available to non-residents, such as beach access, street parking, and special sewerage and garbage removal services. This exclusivity comes at the cost of higher taxes for district residents.

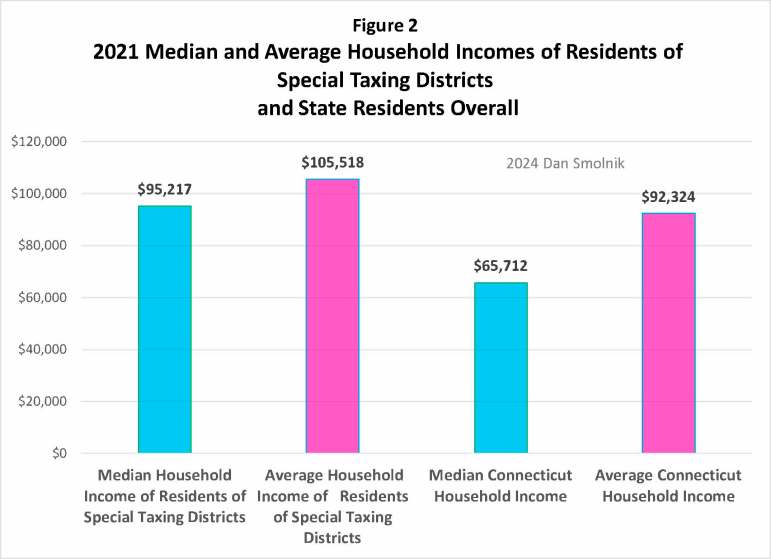

Residents of special taxing districts are wealthier than state residents overall. These districts represent only 45 distinct geographical areas — a fraction of the 169 towns in Connecticut. As shown in Figure 2, household income of the residents who self-select into special taxing districts is an average of 13% higher than the state average and 45% higher than the state median. For perspective, this amount puts these residents into the next higher income quintile.

Improvement associations and beach and lake associations comprise the most common uses to which special taxing districts are dedicated. Over 63% of all the special taxing districts in the state are dedicated in this way to the distribution of public services to private purposes.

As Connecticut’s special district numbers have grown over time, so has the inequality of our income distribution. The level of dispersion of wealth, expressed here as a Gini index, has remained persistently higher than that of the country, as illustrated in Figure 3.

Connecticut’s persistently high, and rising, polarization of income, juxtaposed with its 11% increase in population since 1992, inform us that wealth is moving into the state.

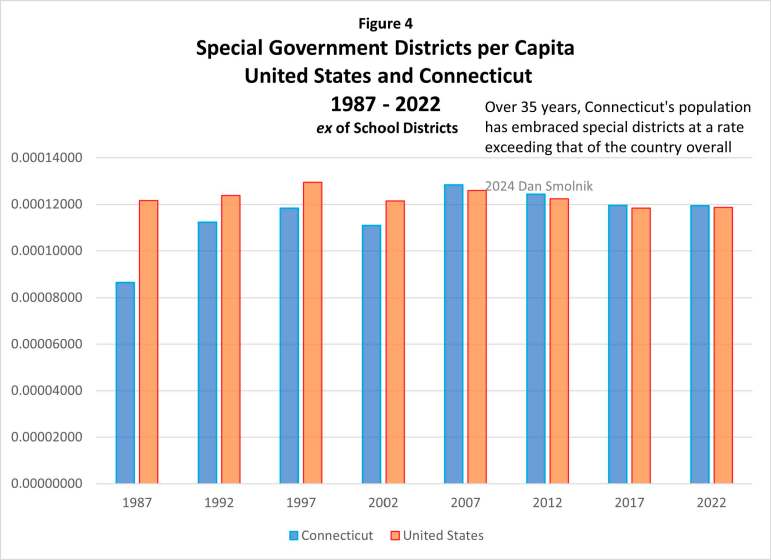

The increasing self-sequestration of Connecticut residents into special taxing districts can be inferred from the data shown in Figure 4.

Over the last two decades, the number of special taxing districts per capita has increased over 6%, while nationally this figure has declined over 4%. This paradoxical phenomenon recapitulates the dramatically higher income polarization in Connecticut as compared to the country overall. Towns can anticipate that residents of these bastions of wealth will defend that wealth, especially insofar their special district provides them continued value.

Hence, Connecticut’s rising population juxtaposed with the growth in the numbers of havens for its wealthy, suggests the development of an economic distortion, wherein sub-municipal, largely secluded, residential political entities thrive without the symmetric effects of taxation and resources affecting their residents’ allocative decisions.

In short, as they presently exist, Connecticut’s special taxing districts, while undoubtedly shifting the costs of access to certain resources to the residents who elect to enjoy them, also appear to perpetuate that access. Insofar as those residents apprehend their wealth as being bound up in their exclusive access the district related amenities, they also magnify the polarization of that wealth, even within towns.

Dan Smolnik is a tax attorney in Hamden and serves on the Hamden Economic Development Commission. He also serves as a board member of the Connecticut Economic Development Association (CEDAS). Any views expressed are exclusively those of the author.