Years ago, when I was reporting on health care for The Connecticut Mirror, it was hard to get through a week without hearing about trouble brewing in the long-term care insurance industry.

Frustrated policyholders packed informational forums at the state Capitol and municipal office buildings to complain about exorbitant rate hikes. They streamed into legislative hearings to testify on a flurry of bills meant to offer relief. Lawmakers tried in vain to push solutions through the General Assembly.

Insurers acknowledged miscalculations had been made when plans were created, but now argue rate increases are necessary to keep policies afloat.

In 2023, my colleagues and I decided to investigate.

We learned there was no database where we could compare rate hike requests and approvals, so we built one. To understand the extent of the problem in Connecticut, we calculated how many policyholders had experienced rate increases of 50% or more, discovering that more than 17,000 people were affected.

There were a mountain of bills considered by the legislature and hundreds of complaints filed with the state to sort through. And we looked at policy in several other states to grasp what others had done about it.

[READ THE INVESTIGATION: CT long-term care insurance costs are skyrocketing, strangling consumers]

People bought these insurance plans to make sure they could get good care as they reached old age — their most vulnerable years — but as the cost of annual premiums kept rising, coverage was becoming less affordable, and many policyholders struggled to hold on or were forced to drop it. Residents reported paying five, 10 — sometimes 15 — times more per year for policies now than when they purchased the coverage decades ago.

Here’s how we set about investigating the long-term care industry:

Grievances. We submitted a public records request for complaints about long-term care insurance going back to 2018, the farthest back the state Insurance Department kept records. We received and reviewed hundreds of grievances — the department had received 769 as of publication time — to get a broad understanding of policyholders’ plight. The frustration was palpable.

“It is the elderly, those who have paid and paid and worked their whole lives who are victims here,” one person wrote.

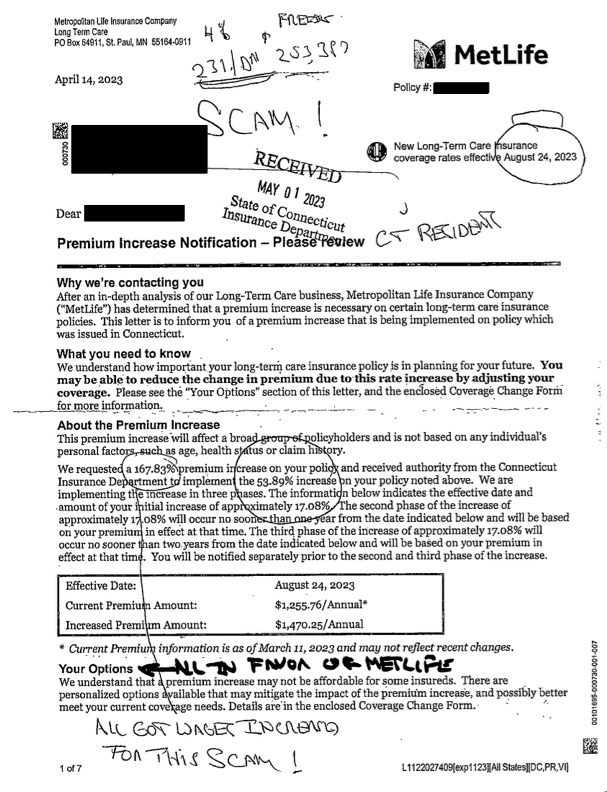

Another, who was facing a 54% premium increase, wrote “SCAM!” across the top of a letter from their insurance provider and sent it to state officials.

We interviewed dozens of these consumers.

Rate hike analysis. State officials don’t publicize annual rate hike requests and approvals for long-term care insurance policies as they do with health care plans. Many residents have inquired about trends in rate increases — how often does the Insurance Department approve them, and by how much? While the agency does post records on its website, they are often voluminous and hard to decipher.

CT Mirror Health Reporter Katy Golvala spent months going through hundreds of documents to analyze six years’ worth of rate requests and approvals. Her review found that more than 17,000 people had received rate increases of 50% or higher, and a few dozen were dealing with hikes as high as 174%.

Some of the biggest companies in the market, including Genworth Financial, Metropolitan Life Insurance Company and Transamerica Life Insurance Company, requested rate increases for five years in a row beginning in 2019.

In 2022, Genworth raised rates for more than 2,000 people by an average of 97%, with increases ranging from 79% to 173%, depending on the policy. The approved amounts were a slight reduction from the company’s original request.

Legislation. Our team also built a database of all the long-term care insurance bills introduced from 2019 to 2024, and we tracked how far each piece of legislation made it through the General Assembly. The proposals were numerous, though only a few won passage. Over the last six years, more than 50 bills have been introduced. In 2023 alone, lawmakers raised 15 proposals.

At least three have passed since 2019. It’s possible some measures that died in committee were tacked onto another bill or included in the state budget, but we could find no instances where that occurred.

Many of the proposals that were shelved focused on tax credits for people with long-term care insurance, while others included caps on rate increases, the requirement of a public hearing for rate hike requests, and notifications for consumers about the risk of rising premiums.

We read through hundreds of pages of written testimony and watched legislative hearings to understand support for and opposition to these measures.

SEC records. The CT Mirror reviewed records filed with the U.S. Securities and Exchange Commission and transcripts of earnings calls for one of the largest providers of long-term care insurance, Genworth Financial, to learn about executive pay and the company’s relationship with state regulators across the country.

Genworth’s business plan relied heavily on the company getting what it wanted from insurance regulators. In 2015, Genworth began reporting to investors every quarter how many rate hikes it got approved and the average of those increases for their long-term care insurance plans.

The documents offered insight into a top company’s strategies.

Policies in other states. We examined a new program in Washington state that provides long-term care coverage for residents through a payroll tax. At least 18 other states have considered similar initiatives; we reviewed legislation and other proposals in those places.

We also looked at tax incentives offered in other states and bills raised to limit rate hikes.

Other efforts. We studied state data on the number of in-force long-term care insurance policies going back to the 1990s, watched informational forums on the issue, talked to insurance experts and elder care advocates, and reviewed court records.

By connecting with more than 50 people, reading through thousands of pages of documents and analyzing hundreds of data points, we were able to piece together a comprehensive picture of the problems with long-term care insurance in Connecticut.

After our project ran, key lawmakers said there is an urgent need to reform the system for Connecticut residents. They are considering at least 14 bills on the issue, including a broad measure recently introduced by members of the Insurance and Real Estate Committee.

Got a tip about long-term care insurance? Please email jcarlesso@ctmirror.org.