The earnings from Wall Street that have buoyed Connecticut’s budget for decades haven’t been flowing at quite the same level since the recent recession, much to the dismay of the governor.

And after watching investment earnings underperform for most of the last three years, Gov. Dannel P. Malloy is hoping that Connecticut’s once-predictable cash cow known as Wall Street is finally returning to form – just in time for his re-election bid.

But while several prominent Connecticut economists say the state’s investment-related tax receipts may well be on the upswing, they are skeptical that Wall Street will fully match the gains it offered in decades past, and some say the state will be in trouble if it doesn’t lower its expectations.

‘Boom-Boom ’80s and ’90s’ aren’t back yet

“The potential for there to be more (investment earnings) is certainly there,” Peter Gioia, chief economist for the Connecticut Business & Industry Association, said last week. “But I would agree than in the next seven or eight years, we still will not be back to the boom-boom ’80s and ’90s. We still have a lot of recovery to go through.”

Fred V. Carstensen agreed. The University of Connecticut professor who heads the school’s economic think-tank said, “We have a lot of wealthy individuals, venture capitalists and hedge funds. They rack up a lot of capital and generate a lot of revenue.

“But I would be skeptical of any claims it is going to be sustainable” at pre-recession levels.

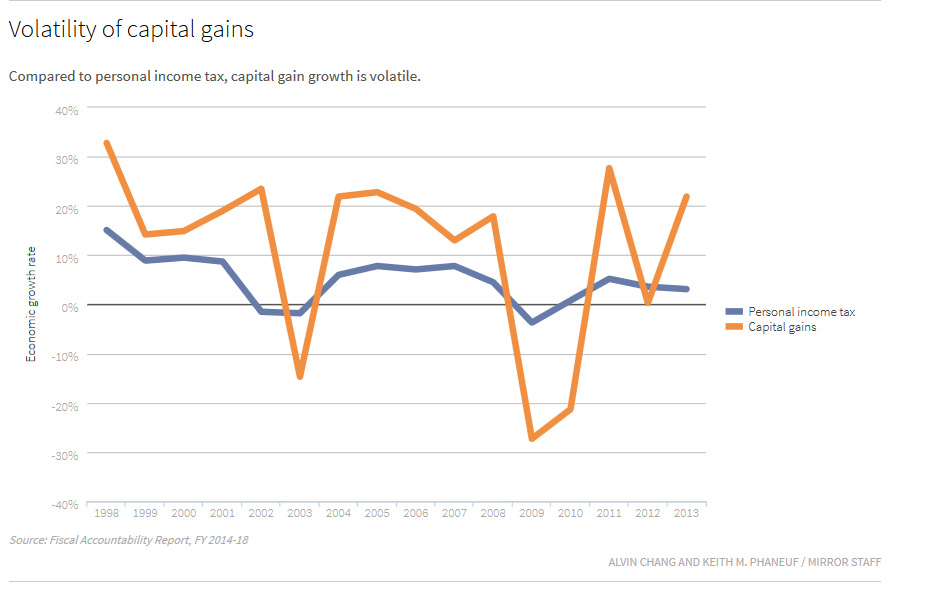

State government’s single-largest source of revenue is its income tax, which provides about $9 billion, or half of its annual operating budget. While most of its income tax receipts come from regular withholdings from residents’ paychecks, nearly 40 percent come from capital gains, dividends and other investment earnings.

And while withholdings are predictable and shift modestly – in good and bad times – capital gains used to be just the opposite.

Between 2004 and 2008, Connecticut’s income tax receipts from investments grew an average of 20 percent each year. Over those five years combined, Wall Street’s contribution to the state’s coffers jumped by almost $2 billion.

In the first two years of Malloy’s term, actual receipts grew, on average, by 14 percent per year. But — if you omit revenue changes tied to political decisions on Capitol Hill, and just consider pure market forces — the average annual increase was just 11 percent.

And what Malloy has gotten from Wall Street was largely used trying to fill the enormous $3.7 billion budget deficit he inherited when he took office in 2011. That gap was equal to nearly 20 percent of Connecticut’s annual operating expenses.

The administration had initially assumed Connecticut’s recovery would largely mirror those from past recessions, but again and again, it was forced to downgrade its expectations. Revenues grew and the economy improved during its first two years, but nowhere near the pace the governor and legislature were counting on to support the budgets they adopted.

Good news, bad news in 2013

But 2013 finally brought Malloy his first rays of hope.

Investment-related income tax receipts surged. But was that because the markets were improving? Or was it because wealthy residents – anticipating the end of the Bush-era tax breaks – sold their stocks in late 2012 so their gains could be taxed at lesser, expiring federal income tax rates?

Still, the stock market gained about 25 percent in value in 2013, and Gioia said that can’t be dismissed.

“That’s a big number,” he said. “That will certainly have some impact” on state tax receipts in the near future.

Retired Fairfield University professor Edward Deak, who prepares the New England Economic Partnership’s Connecticut forecast, agreed that the growth in equity markets is a very healthy sign.

But he added some cautionary notes.

The last recession made long-lasting structural changes to the state and national economies.

Businesses now use technology and capital as never before to replace jobs. These efficiency moves causes profits and market values to rise, Deak said, but don’t necessarily help businesses add customers or expand.

“These types of moves actually suppress innovation,” Carstensen said. “The full run of corporate profits we saw last year just doesn’t seem to be entirely sustainable.”

“There was a real attempt to control the bottom line in 2013,” Deak said. Something as simple as a retail chain’s keeping inventories low during the last holiday shopping season might have propped up its profits and its standing on the stock market, he said. But it doesn’t represent true business growth, and some of that equity market value could easily disappear.

In addition, Wall Street has shed thousands of jobs, and the financial services sector of the regional economy likely won’t ever return to pre-recession levels, Carstensen said.

What’s more, the markets also benefited last year from the Federal Reserve Bank continuing to hold down interest rates. That will likely begin to change by late 2014 or early 2015, Deak said.

Malloy stays upbeat

While economists find good and bad signs in a recovery they predict will continue for several more years, Malloy has continued to emphasize the positive side.

“We are seeing real (revenue) growth,” he said last week. “We are meeting targets. We are exceeding targets.”

Most of what Malloy is referring to just happened recently.

And two years of adopting budgets and watching revenues grow too little to meet targets, the administration got nonpartisan analysts to agree in mid-January that numbers had swung the other way.

With Wall Street-related earnings leading the way, analysts project a surplus of more than $500 million in the current budget and about $160 million for the fiscal year that begins July 1.

Still, those surpluses are deceptive.

That’s because Malloy and the Democratic-controlled legislature used borrowing and other gimmicks to delay paying hundreds of millions of dollars in operating expenses for this budget and the next. Those bills — plus interest — will come due after the election in November.

Nonpartisan analysts for the legislature project that the first budget written after the election will very likely start with a $1 billion deficit.

And that forecast assumes that Connecticut’s economy – and its help from Wall Street – will grow quite a bit between now and then. State income tax receipts have to grow by almost $500 million over the next year just to keep the post-election deficit from getting larger.

“Wall Street is a blessing and a curse,” said Rep. Vincent J. Candelora, R-North Branford, a veteran member of the tax-writing Finance Committee and one of the most vocal critics of Malloy’s budgets.

Candelora said the deficit Malloy inherited – and many related problems – were created during the 1980s and 1990s because officials didn’t think the Wall Street money would ever stop growing. They would be better served now, Candelora said, to expect a more modest return in the future.

“We can’t count on that again,” he said. “There is a new normal.”