There’s been a new twist in the debate surrounding Connecticut’s cash-starved pension fund for state employees.

Is it a ticking time bomb whose exploding costs, if not diffused soon, could threaten taxpayers by the early 2020s.

Is it an emergency fund state officials could tap one last time to help with the current budget crisis?

Or possibly both?

With proposals for a retirement incentive program — which strengthens the budget but weakens the pension fund — already on the table, Senate Democrats indicated their willingness to consider a move that could significantly reduce deficits within the next fiscal year or two, but at considerable expense to the pension system.

“I think for anyone who claims they are trying to solve the current deficit, those claims come into doubt if they’re not recognizing that short-term budget fixes create long-term pension problems,” House Speaker J. Brendan Sharkey, D-Hamden, said Monday. “There’s ample evidence of that over the last 20 years.”

Sharkey is referring to a pension fund that holds enough assets to cover less than 42 percent of Connecticut’s long-term obligations to its workers and retirees.

“We didn’t get to the situation we are in overnight,” he said, “and we’re not going to solve that problem in a fortnight.”

The fund’s incredibly poor health is primarily the product of decades of inadequate savings by governors and legislatures before 2011. But it also stems from periodic state programs that produced a huge surge in worker retirements.

To mitigate this pension crisis, Gov. Dannel P. Malloy proposed a new payment structure back on Oct. 28.

The plan effectively spares the state from billions of dollars in required pension contributions between 2019 and 2032. The burden of making those contributions — and recouping the investment earnings they otherwise would have garnered — would fall on state budgets for a decade or two after 2032.

Unless future generations bear some of this cost, the administration argues, this year’s $1.5 billion pension fund contribution could double by 2025 and more than quadruple by 2032. This would force huge tax hikes and drain resources from vital state programs.

But the governor’s plan would not begin shifting any costs into the future until 2019. In fact, it temporarily increases pension expenses facing the state in 2017.

At the same time the governor put this issue on the table, he also challenged legislators to help him solve the more immediate problem of budget deficits.

According to nonpartisan legislative analysts, this fiscal year is $254 million in deficit. The projected shortfall grows to $552 million in 2016-17, and $1.72 billion in 2017-18 — the first new budget after the next state election. That last deficit represents a gap of 8.5 percent of annual operating costs.

And while legislators from both parties have pitched a wide array of budget-balancing moves, a few would wipe away red ink while worsening the massive pension bill looming in the future.

Republicans in both chambers and Senate Democrats all favor offering senior state workers incentives to retire.

They estimate this would save the budget about $80 million this fiscal year.

The theory behind that is simple: Senior workers retire sooner than they planned — relieving the state of their higher salaries. Some positions are refilled with lower-paid, less-experienced workers, and others are left vacant to maximize savings.

But it also means some employees who otherwise would be working – and paying into the pension system – instead are retired, and drawing funds out of the system. This expense is compounded year after year, since it also means the pension system has fewer dollars with which to earn investment returns.

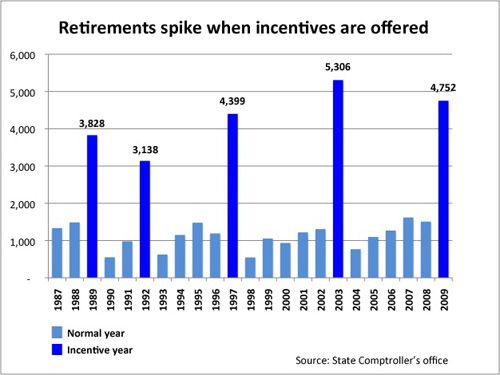

Retirement incentive programs, though controversial, nonetheless were a popular choice among prior governors and legislatures to cut personnel costs during tough fiscal times, having been offered five times since 1989. A sixth – estimated to save about $88 million – would have been made available in 2010 had state union leaders accepted a proposal from then-Gov. M. Jodi Rell.

During those two decades, annual retirements in years without incentives average 1,117. By comparison, in years with incentives retirements averaged almost four times as much, or 4,285 workers.

Union leaders have been increasingly wary of retirement incentive programs since then, often citing the worsening health of the pension fund.

Malloy has steadfastly refused to support retirement incentives because of their impact on the pension fund.

Senate Minority Leader Len Fasano, R-North Haven, recently defended the inclusion of retirement incentives in the Republican budget-balancing plan as a reasonable compromise.

Though he acknowledged the incentive plan could impact the pension fund, Fasano noted it is more modest than past proposals. Unlike its predecessors, these incentives would be offered only to workers already eligible to retire, and not to those a few years away from eligibility.

The GOP also proposed a wide array of worker benefits-related cost-saving measures, including higher pension contributions and health insurance premiums for employees, caps on cost-of-living adjustments to pensions and an end to longevity pay for senior workers. These concessions would have to be negotiated with employee unions.

And while majority Democrats in the Senate backed the retirement incentive plan, their House counterparts did not.

“Every economic expert knows that a retirement incentive program, despite some short-term savings, can wreak havoc on long-term fiscal health,” Sharkey wrote in a joint statement with House Majority Leader Joe Aresimowicz, D-Berlin, adding this concern was reiterated in a recent study of state pensions by a Boston College think tank.

But last Friday the question of easing budget deficits at the pension fund’s expense took a new twist.

Senate Democrats broke with House Democrats to offer their own budget-balancing plan.

Besides including retirement incentives, the Senate Democratic plan also listed, among its highlights, restructuring the pension system.

Malloy’s restructuring didn’t save state finances any money until 2019. Why did Senate Democrats suggest pension restructuring in a plan aimed at balancing state finances this fiscal year and in 2016-17?

Would Senate Democrats consider shifting pension costs from the current biennial budget into the future?

The caucus hasn’t developed a specific proposal, but Senate President Pro Tem Martin M. Looney, D-New Haven, made it clear Senate Democrats hadn’t ruled anything out.

“If there is a savings, we would have to look at it,” Looney said, noting that any pension changes probably would have to be negotiated with the unions.

The administration projects the governor’s plan would save the state budget hundreds of millions of dollars annually at first, and eventually billions per year, by restructuring pension payments. But none of the cost-shifting would begin until 2019, and savings close to $1 billion per year wouldn’t start until 2030.

The top Republican in the House, Minority Leader Themis Klarides of Derby, was skeptical Republicans would be comfortable reducing pension payments now to ease the current budget crisis.

Though Comptroller Kevin P. Lembo and Treasurer Denise L. Nappier also are developing proposals to restructure pension payments, Klarides said that, among Republican legislators, “it’s safe to say there are serious concerns” about the overall concept.

“Whenever we talk about making structural changes to our finances, we don’t want to make the problem worse down the road,” she said. “That’s certainly not something we’re interested in philosophically.”