Psychiatrists tell stories of suicidal patients being required to get prior authorization from their insurance company before being admitted to a psychiatric hospital. Advocates talk of patients struggling to find a mental health clinician who accepts his or her insurance plan.

Some see it as a sign that insurance companies don’t treat mental health or addiction treatment as they would physical illness – despite a federal law requiring it.

But some also acknowledge that it’s not clear whether those stories represent isolated cases or show a pattern of practice that violates federal law.

“Real data about the experiences of patients and doctors is necessary,” Dr. Reena Kapoor, president of the Connecticut Psychiatric Society, said in written testimony to legislators.

It’s a view shared by other practitioners, mental health advocates, the insurance industry and the Connecticut Insurance Department, which has been collecting a wide range of data on mental health coverage. But while providers and advocates have embraced a legislative proposal that calls for a working group led by the Connecticut Insurance Department to gather data comparing approval and denial rates for certain behavioral health and medical services, health plans oppose it, saying lawmakers should allow other recent laws and data collection efforts to develop before imposing another requirement.

To some, it points to the difficulty of testing whether parity requirements are being met.

“I think we’ve been grappling, the plans have been grappling with it, consumers have been grappling with it, regulators I think were grappling with it for a while,” said state Healthcare Advocate Victoria Veltri. “The regulation’s very clear on its face. It’s just not so easy in application.”

“Nobody’s found the magic formula yet,” she added.

The Paul Wellstone and Pete Domenici Mental Health Parity and Addiction Equity Act of 2008 prohibits insurance plans from placing more restrictive limits or costs on mental health and substance abuse services than those imposed on medical and surgical services.

Some aspects are straightforward: It largely ended the practice, for example, of limiting the number of outpatient therapy visits a patient could receive (those would be allowed only if a plan puts the same limits on “substantially all” outpatient medical and surgical benefits).

But others can be murkier and harder to assess, according to practitioners, advocates and researchers, particularly “non-quantitative treatment limits.” Those are things like decisions about whether a service is medically necessary, policies about whether patients must try lower-cost therapies before costlier ones are covered, or decisions about whether patients need advance authorization before treatment will be covered.

The federal parity regulation doesn’t require those standards to be the same for behavioral health services as for medical and surgical care, but requires that “the processes, strategies, evidentiary standards, and other factors used…are comparable to and applied no more stringently.” The regulation notes that “disparate results alone” don’t mean that the particular limits in use don’t comply with the requirements.

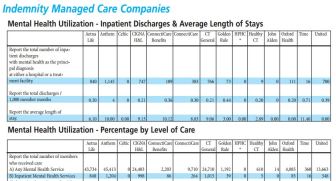

The Connecticut Insurance Department already collects data on a wide range of behavioral health coverage measures – including each carrier’s rates of denials and appeals and the percentage of members who received various types of behavioral health services. It publishes the data in an annual consumer report card. The report card also includes data on medical coverage, but it does not directly parallel the information collected on behavioral health.

The department led a working group on behavioral health last year and is collecting additional data as a result, including information on the authorization and denial of medical necessity by type and level of treatment, and denials that are upheld or overturned.

But Sen. Ted Kennedy Jr., D-Branford, thinks some “essential” data for assessing parity is missing. A bill he proposed calls for the working group to gather data on the number of requests for prior authorization of behavioral health services – and the number of denials – compared to those for other health care services, and the percentage of paid claims for out-of-network behavioral health services compared to other health care and surgical services.

The bill was voted out of the Public Health Committee last month.

In pushing for the data, Kennedy has cited several settlements between health plans and New York Attorney General Eric Schneiderman based on findings that certain plans had denied coverage for mental health or substance abuse treatment services at significantly higher rates than for medical services.

“You can’t do anything about a problem unless you have good data about the issue,” said Kennedy, who said he’s heard many individual stories about difficulties getting coverage for mental health treatment. “And we may surprise ourselves, and it may turn out that we’re actually doing a really good job. We don’t know that, honestly, until we can collect the data from the payers themselves.”

Many mental health advocates and providers say more data is needed, and say their experiences indicate there’s a way to go before achieving parity.

“I think that there is a belief…in this state that we have parity, and I can give you 100 examples of how we don’t,” said Patricia Rehmer, president of the Hartford HealthCare Behavioral Health Network and the state’s former commissioner of mental health and addiction services. She said it’s important to measure not just whether, for example, a plan covers residential treatment, but whether the person can stay as long as necessary or receive appropriate follow-up care after discharge.

But others have questioned the need for legislative action.

The insurance department said in written testimony that the agency already has the authority to gather the data the bill is seeking – so calling back the working group isn’t needed.

And, more broadly, the department believes it can collect the data needed to review and enforce market conduct related to behavioral health coverage, spokeswoman Donna Tommelleo said.

(Kennedy said he’s mainly interested in obtaining the data, regardless of whether it can be done administratively or through the working group.)

In written testimony opposing the bill, the Connecticut Association of Health Plans said the working group process had focused on the need to collect more detailed data from both insurers and health care providers. The association also cited changes made as part of the legislation passed in the wake of the Sandy Hook school shooting, which shortened the timeframes insurers had to review requests for coverage of certain mental health and substance-abuse services from 72 hours to 24 hours, and called for insurers to use more consistent criteria in their coverage decisions.

The association asked legislators to allow that legislation to “fully develop” and focus on data collection consistent with the working group’s recommendations before taking additional action.

Keith Stover, a lobbyist for the association who was part of the working group, said Insurance Commissioner Katharine L. Wade’s efforts to gather data from care providers is important. Often, he said, a provider might cite problems getting a specific service approved for a client, but an insurance company won’t find the same issue after investigating.

“Well, does that mean we’re being unresponsive? Does it mean that our systems aren’t capturing it? Or does it mean that it happens twice in a million claims?” he said. “So if we’re going to be data-driven, if we are going to figure out together, in good faith, policy options, changes in processes, you have to have real data from every side of the transaction.”

From a payer’s perspective, he added, it’s always best to get a person the appropriate care at the earliest possible point. But he said a challenge is that while there are often straightforward protocols on treatment for medical conditions – an X-ray can indicate if a person has pneumonia and what treatment will address it, for example – determining the most appropriate treatment a particular person with a behavioral health condition is often not as straightforward.

Stover said insurers have “absolute commitment to parity,” and said that when issues arise, he’d like those involved to have conversations to address them, rather than “generalizing isolated experiences and making broad policy statements or broad policy demands.”

The working group’s report, issued in February, identified concerns including issues related to the availability of child behavioral health providers in insurance company networks, which the report linked to a shortage of the providers and a reluctance of many providers to take insurance.

On the other hand, many complaints about access to behavioral health treatment received by the insurance department or Office of the Healthcare Advocate were the result of not having the information needed to make a decision about medical necessity, and were resolved when additional documentation was obtained, the working group’s report said.

Veltri, who was part of the working group, said behavioral health issues remain the top reason for complaints to her office. She supports the bill, and she said looking at denial rates for mental health services compared to those for medical services could be a reasonable proxy for assessing whether more investigation is warranted.

Despite the challenges of determining compliance with the federal law, Veltri said she is optimistic. Changes made at the state level have helped, she said, including the provisions of the post-Sandy Hook law and an increased willingness of various parties to work together to address behavioral health coverage issues.

“You wouldn’t normally see a table five years ago that had the insurance department, Office of Healthcare Advocate, Department of Social Services, Beacon [the organization that administers behavioral health services for Medicaid], the carriers and consumer representatives all at the same table, trying to hammer out what we could do, and it didn’t necessarily have to be a bill, but what we could do together,” she said. “And that’s happening.”