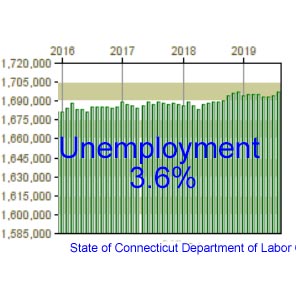

Connecticut added 2,800 jobs in August, but its unemployment rate remained unchanged at 3.6 percent, the state Department of Labor reported Thursday.

The labor department also revised totals this week for July, upgrading the 100-job loss it initially reported last month to a gain of 1,600 positions.

Job gains don’t automatically translate into a reduction in the unemployment rate. That’s because it reflects not only those employed, but also those who are available to work and actively seeking employment.

“We saw gains in six of the 10 major industry sectors,” said Andy Condon, director of the Labor Department’s Office of Research. But “in addition, the labor force grew for the first time in many months.”

Connecticut now has recovered 83.5% or 100,400 of the 120,300 jobs it lost in the last recession, which ran from March 2008 to January 2010.

Connecticut’s private sector has fully recovered, regaining 103.4% or 115,800 jobs against 112,000 positions lost in the last recession.

Don Klepper-Smith, an economist with DataCore Partners, said Connecticut now has gained a modest 400 jobs between December 2018 and August 2019.

“Extrapolating this current growth out in time, we see that the state’s economy is not likely to see full job recovery until mid-2021 based on existing labor market fundamentals,” said Klepper-Smith, who was state government’s chief economic advisor in the late 2000s under then-Gov. M. Jodi Rell. “The odds are that both Connecticut and the nation are apt to be encountering a full-blown national recession prior to full job recovery in Connecticut, which raises serious questions about the state’s fiscal health over the near-term.”

The leisure and hospitality sector grew the most jobs in August adding 1,400 jobs. Gains also were recorded in: professional and business services; other services; construction and mining; trade, transportation and utilities; and government.

The education and health services sector lost the most jobs in August, down 900 positions. Losses also were recorded in the information and manufacturing sectors, while the financial activities sector remained unchanged in August.

Regionally, the Hartford labor market added 800 jobs in August. The Bridgeport-Stamford-Norwalk and New Haven markets each added 600 jobs while the Norwich-New London-Westerly market added 100 positions.

The Waterbury labor market lost 200 jobs last month.

Gaining jobs is not the same as economic growth. The Connecticut;s economy systematically contracted from 2010 through 2017 at about a -1% annual compound rate; 2018 finally saw modest growth–recovering to where we were in about 2004 (measured in real terms, that is, adjusted for inflation). And this jobs report is not particularly encouraging because the largest growth was in the sector with the lowest wages: leisure and hospitality. It would certainly elevated public understanding if we looked simultaneously at economic growth (reported quarterly), withholding tax data (which reveals what is happening to incomes), and the quality of jobs–not just their numbers.

The reality is that Connecticut’s economy continues to struggle; we aren’t seeing anything yet that will deliver solid growth in the output (state GDP) going forward. Ultimately, it is growth in output, not jobs, that will drive improving tax revenues and thus help address the continuing fiscal crisis.

In addition, the private sectors recommendations, made in 17 & 18 to spur growth and send a message to the broader markets about our past mistakes, was largely ignored by politicians who refuse to make some really difficult choices in reducing an unsustainable overall budget. There is very little outside investment coming in and no really large enterprises looking at us seriously. In fact, some that are here now are getting serious about their “plan b” and many are investing elsewhere. Keep an eye on AGI collections because I think Connecticut will have a very difficult time as national GDP slows, obvious we will see a cap gain bump, but then what?Our reserves will help but only in the most extreme cases. GSP growth is anemic, just awful, and would be even worse if not for the defense industry, how ironic. Also there seems to be an awful lot of very nervous people in the markets and a massive amount of dollars have flowed into ETFs. Let’s hope they all don’t run for the exit at the same time.