Connecticut continues to lag most states in saving to meet its pension obligations to public-sector retirees, according to a new report from The Pew Charitable Trusts.

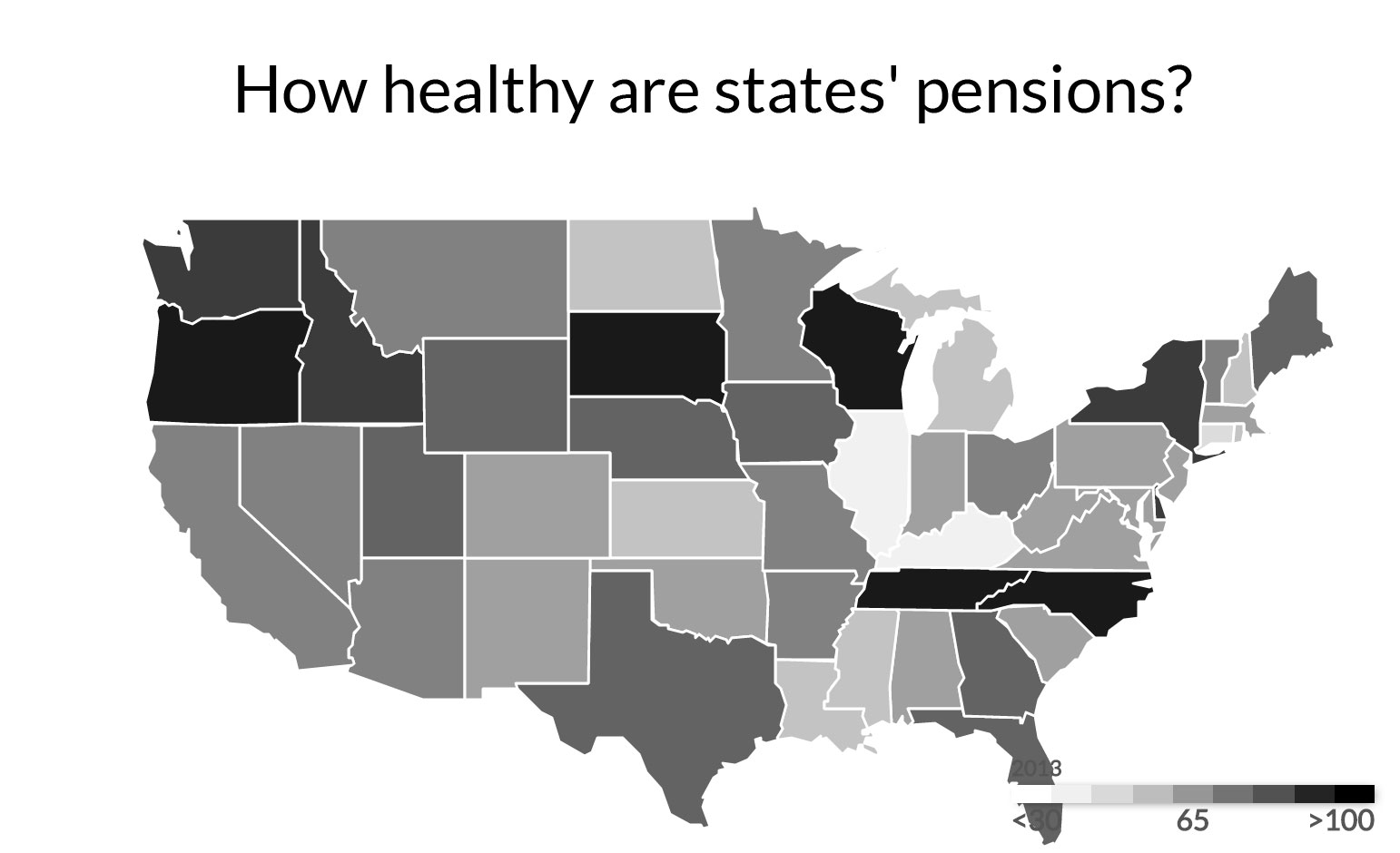

Connecticut had enough assets in 2013 – the year Pew chose to test pension data in all states – to cover just 48 percent of the long-term pension obligations owed to state employees and public school teachers.

It is one of only three states with a funded ratio below 50 percent. Only Kentucky and Illinois ranked lower at 44 percent and 39 percent, respectively.

Fifteen states had an overall funded ratio of 80 percent or higher in 2013, according to the Pew report. Many experts say a healthy pension program should have enough funds to cover at least 80 percent of its long-term obligations. South Dakota and Wisconsin ranked highest in 2013, each with 100 percent funding.

Connecticut has taken steps in recent years to improve its pension savings habits. And it and other states have experienced healthy investment returns since 2013.

But the report cautions that aggregate pension debt among all states — $968 billion in 2013 and likely close to $900 billion today — remains a huge concern.

This debt “will remain higher as a percentage of U.S. gross domestic product than at any time before the Great Recession,” the Pew report states. “State and local policymakers cannot count on investment returns over the long term to close this gap and instead need to put in place funding policies that put them on track to pay down pension debt.”

State employees pension has big unfunded liability

Connecticut has taken steps in recent years to bolster its pension programs. But some haven’t worked exactly as planned, at least in the early stages.

Gov. Dannel P. Malloy and the legislature approved a plan in the spring of 2012 to ramp up payments for more than a decade into the state employees’ pension system.

That fund has suffered from an array of questionable fiscal policies since it began in the mid-1980s with a huge financial hole. For nearly four decades before that, Connecticut had put nothing away, and therefore gained no investment earnings to help cover state workers’ pension costs.

Several early-retirement programs and pension fund raids under previous governors and legislatures to help balance the state budget also weakened the fund.

The state employees’ pension emerged from the Great Recession with a 42 percent funded ratio by mid-2012 – just after Malloy’s pension fix was approved – but it still fell to 41.5 percent two years later.

That’s because the labor concessions package the governor secured from unions in 2011 – which reduced retirement benefits – also gave workers a brief window during which they could retire and avoid those restrictions.

More than 2,600 state workers took advantage of this and retired during the first three-quarters of 2011, about 2½ times the number recorded at that point in the previous year.

Mass retirements tend to weaken pension funds, Workers, who would be paying into the pension fund, become retirees who draw dollars out of the fund.

Pew drew national attention in 2007 with the first of several reports highlighting states’ growing struggles to save for pensions and other retirement benefits owed public-sector workers. Connecticut also has lagged most states in retirement benefit savings in earlier reports.

“It’s clear that Pew is trying to get the attention of governors who haven’t gotten it yet that they need to deal with their pension liabilities,” said GianCarl Casa, spokesman for Malloy’s budget office. “Here in Connecticut, Governor Malloy gets it and has been acting consistently to take care of the problem over the last four-and-a-half years.”

Casa added that “under Governor Malloy, Connecticut has been funding 100 percent of its annual required contribution, something that was not always the case before he took office. Taken in combination with changes in benefits that he negotiated, Connecticut is on track to fully fund our pension system in about 15 years. We have made our pension system more affordable and we are keeping our commitments – at a time when other states are not.”

Teachers’ pension got a boost from bonding

Connecticut’s pension fund for public school teachers also had suffered from decades’ worth of inadequate contributions. It had just 63 percent of its obligations funded in 2007 when the legislature and then-Gov. M. Jodi Rell approved Treasurer Denise L. Nappier’s plan to borrow $2 billion through bonding and deposit it into the pension fund.

The assumption was that the investment return on those borrowed dollars would average more than 8 percent annually over the next two decades, while the interest on the bonds would be just over 5 percent.

As part of its contract with the investors that bought Connecticut’s bonds, the state promised to make the full contribution recommended by teachers’ pension fund analysts for the life of the bonds.

“We were the only known pension fund with that policy at the time, ensuring full funding,” Nappier said, adding this bond covenant guarantee was crucial “to rid ourselves of the undisciplined actions of the past.”

The teachers’ pension borrowing plan can’t be judged fully until after the bonds are paid off more than a decade from now. Shortly after the bonds were issued in 2008, Connecticut and the nation fell into recession, and the value of teachers’ pension fund assets dropped in the short-term.

The teachers’ pension had a funded ratio of 70 percent in 2008, after the bonds were issued. It fell to 61 percent in 2010 and 55 percent in 2012 before climbing back to 59 percent in 2014.