This story is part of CT Mirror Explains, an ongoing effort to distill our wide-ranging reporting into a "what you need to know" format and provide practical information to our readers.

Editor’s Note: This article is part of CT Mirror’s Spanish-language news coverage developed in partnership with Identidad Latina Multimedia.

The General Assembly and Gov. Ned Lamont recently approved one of the largest state tax cuts in Connecticut history, with total relief worth approximately $500 million per year by 2025.

Part of that package expanded existing exemptions and other tax breaks for retiring income, involving pensions, annuities and individual retirement accounts.

Here’s an up-to-date guide outlining Connecticut’s current tax exemptions on retirement income. (These exemptions apply only to state income taxes, not federal taxes.)

Social Security

Connecticut exempts from state taxation the same amount of Social Security income that the United States government exempts from the federal income tax — and it may exempt more as well, depending on a filer’s annual income.

The state exempts 100% of federally taxable Social Security income for single filers and married people filing separately whose federal adjusted gross income is below $75,000 a year, and for couples filing jointly with an AGI below $100,000 annually.

Taxpayers whose AGI exceeds those limits qualify for a partial exemption, with no more than 25% of their total Social Security benefits subject to taxation.

Military and Railroad Retirement Pay

Fully exempt from state income tax.

Teachers’ Retirement System

All retired municipal teachers can deduct 50% of their pension income.

However, some may be eligible for a general pension and annuity exemption larger than the teachers’ retirement deduction (see eligibility requirements below). Those retired teachers can claim that exemption instead.

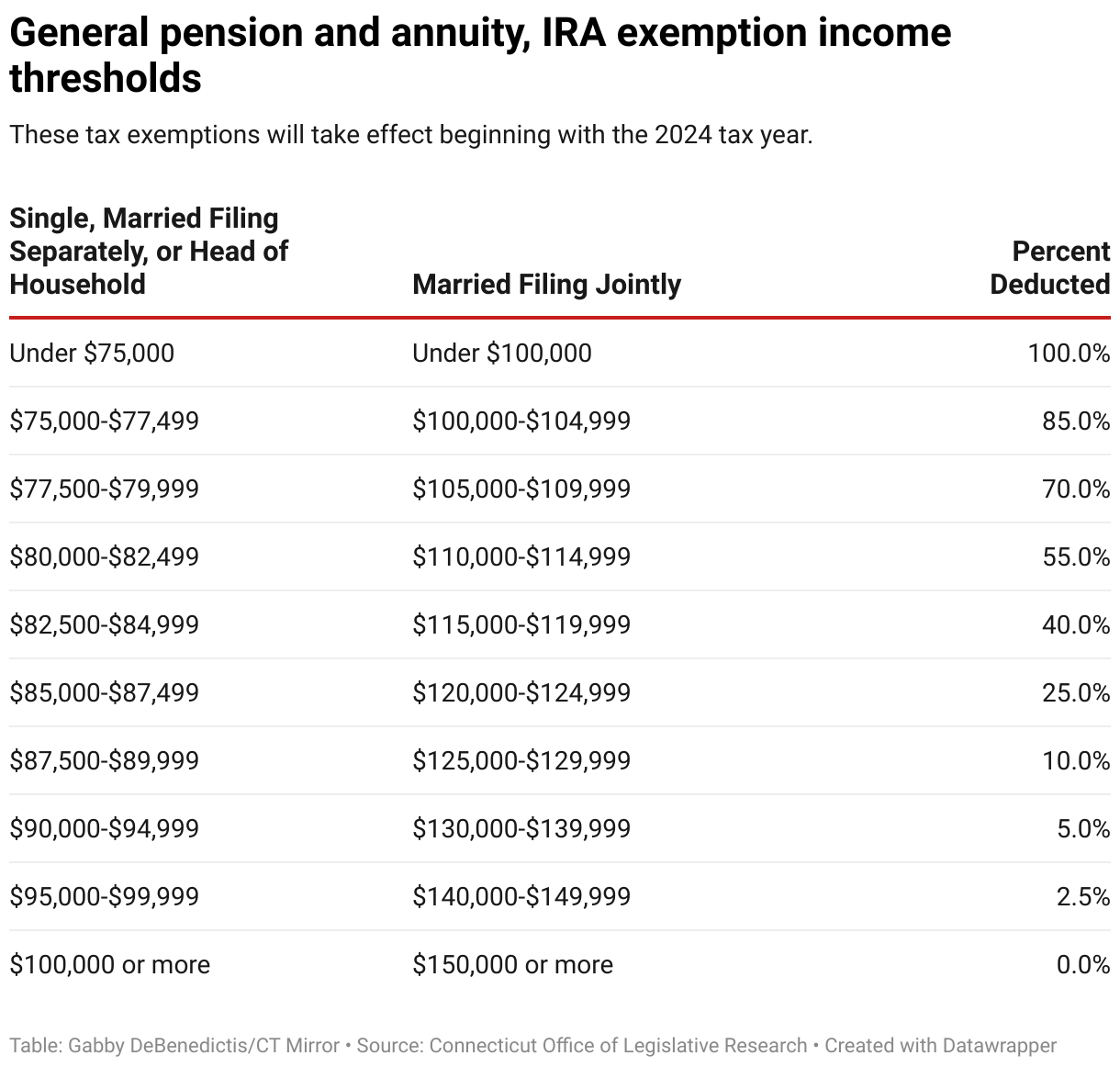

General Pension and Annuity

General pension and annuity earnings are 100% exempt from income taxes for single filers and married people filing separately with an overall AGI of less than $75,000 a year. Couples filing jointly with an AGI of less than $100,000 a year are fully exempt as well.

Historically, anyone with an income above those limits did not qualify for any exemptions on general pension and annuity earnings. But lawmakers modified that in this year’s state budget, and beginning in the 2024 tax year, some retirees with higher earnings will qualify for exemptions on a sliding scale.

Single filers and married people filing separately with an AGI between $75,000 and $99,999 can exempt a percentage of their income from taxation, as can married people filing jointly with an AGI between $100,000 and $149,999.

Details on those exemptions can be found in the chart below:

Individual Retirement Accounts

Beginning in the 2024 tax year, IRAs, excluding Roth IRAs, will be subject to the same tax exemption income thresholds as general pension and annuity income. (See chart above for those exemption levels).

And each year from 2024-2026, the state will increase the percent of IRA income that can qualify for an exemption. (Currently, only 25% of IRA income qualifies.)

In 2024, 50% of one’s IRA income will qualify for an exemption, and that number will rise to 75% in 2025 and 100% beginning in 2026.

That means that during the 2024 and 2025 tax years, eligible filers can exempt their qualifying percentage from each year’s percentage of tax-exempt IRA income.

For example, a person who makes $77,000 annually is eligible to exempt 85% of their IRA income from state taxation. But in 2024 only 50% of IRA income is eligible for a tax exemption, so that person can only exempt 85% of the eligible 50%.