This story is the latest in a series on how to better navigate the health care system.

For many Americans, the days of paying a $10 or $20 copay for a doctor visit and leaving the medical bills to their insurance companies are long gone. Instead, many are paying a larger share of their medical bills, often through deductibles that leave people to pay the full cost of care until they hit a certain dollar limit. And that means not just higher potential costs, but more to understand – from figuring out how much care costs to handling bills that aren’t always clear.

What can people do to better manage their high-deductible plans? Here are some tips from experts.

Know what your deductible applies to.

The basic premise of a deductible: You pay the full cost of care until you reach a certain dollar limit, at which point the plan begins chipping in.

But deductibles work differently depending on the plan. In some cases, they apply to all care (with the exception of certain preventive services; more on that below). In other cases, they only apply to certain services – often, hospitalizations or imaging are included – but don’t apply to doctors’ office visits. Some plans have separate deductibles for medical care and prescription drugs.

Deductibles also vary in how they apply to family plans. Take, for example, a plan with a $1,000 deductible for individuals and a $2,000 deductible for families. In some family plans, any one person would only have to meet the $1,000 individual deductible before the plan begins paying toward his or her care. The family would remain responsible for the other covered family members’ expenses until they incur enough costs to meet the remaining $1,000 on the deductible. In other plans, the full family deductible could be met by any individual family member or multiple people.

If you’re not sure how your deductible works after you read your plan documents, call your insurance company’s member services number and ask.

Know what’s covered at no cost, no matter what your deductible is – and know the exceptions.

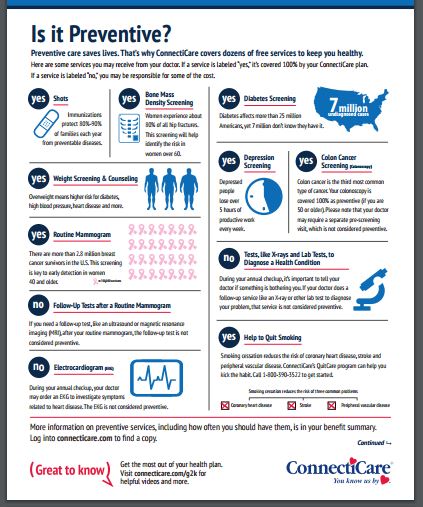

Under the federal health law, insurance plans must cover certain preventive services at no charge to the member – regardless of whether they have a deductible or not. Here’s a list of those services.

But there’s a big caveat to know. In some cases, patients have gone for what they expect to be a no-cost preventive visit and have ended up with a bill. That’s because if they address issues that go beyond the scope of a preventive visit, the doctor’s office can bill them for a different type of visit that isn’t fully paid for by their insurance plan.

State Healthcare Advocate Victoria Veltri said unexpected bills for what began as preventive care are an increasingly common complaint topic for her office.

“For people who are price-sensitive, they need to ask questions,” she said. She suggested telling the doctor or office staff that you’re coming in for a free preventive visit and want to be sure to know if anything happens that will lead to you getting a bill.

Ideally, she added, doctors would let patients know if the visit moves beyond the covered services in a free preventive visit, even if it’s in the patient’s best interest to address whatever additional issues come up.

“I think it should work from both ends,” Veltri said. “Providers should provide that information, and I think the patient should ask the question.”

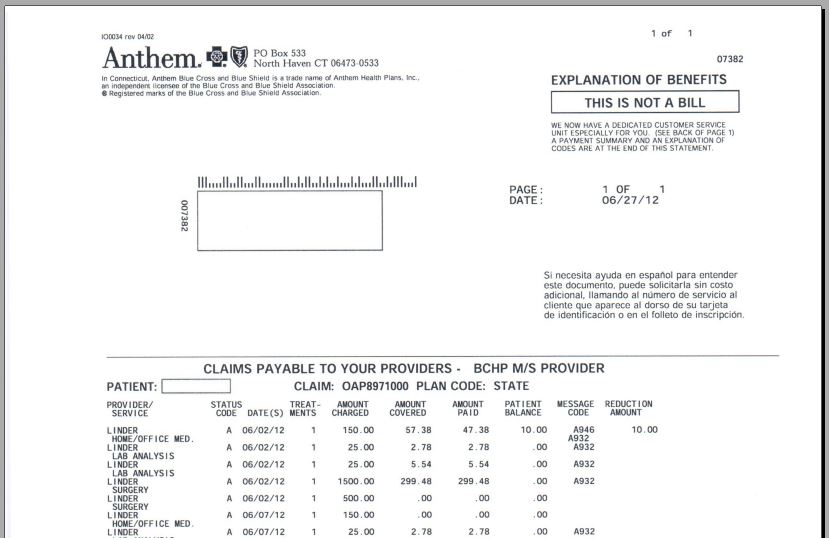

Learn to read your ‘explanation of benefits.’

Having a high deductible means you’re more likely to deal with medical bills directly. And that means you’ll have to figure out what you really owe – which isn’t always easy. While providers might charge a certain amount, the figure that usually matters to you is what amount your insurer has negotiated with the provider.

Experts say you should look not just at your bill but at the “explanation of benefits” form you get from your insurance company. That form will let you know how much was billed, what the insurance plan paid, and what you owe. Kathy Walsh, principal examiner in the Connecticut Insurance Department’s Consumer Affairs Division, advises people to save explanation of benefits forms and compare them to any bills they receive from health care providers. If they don’t match, call the provider or the insurer.

For more on how to read explanation of benefits forms, including samples from various insurers, click here.

Check your medical bills closely.

“Many people will scrutinize their other bills very carefully before they will scrutinize a hospital or provider bill, or even an explanation of benefits from their insurance company,” Veltri said. “My advice to people is to use the same level of scrutiny that you’d apply if you thought you had a $5 overcharge on your cable bill.”

In some cases, providers send bills before the claim has been settled with the insurance company – meaning the patient might get billed for what the insurer would pay, Veltri said.

She recommended checking the explanation of benefits to make sure it lists the correct provider, date of service and the services you got.

And she advised people not to pay until they’ve reviewed both the bill and corresponding explanation of benefits – and ensured that the charges are accurate.

Be prepared to pay up-front.

In some cases, health care providers require patients with deductibles to pay a portion or all of what they’ll owe ahead of time, particularly if they’re planning costly services like surgery or a hospital admission.

“People have to think of it like it was in the old days with a copayment,” Walsh said. In other words, paying up front, but in this case, it could be significantly more than a $30 or $40 copay.

Save up.

People with qualifying high-deductible plans can use health savings accounts to save money on a pre-tax basis to use for their health care expenses.

“That’s a good way to try to help budget the expenses that they have to pay for toward their deductibles, as well as utilizing those tax-free dollars,” Walsh said.

To avoid surprises, try to learn the cost of care ahead of time.

In some cases, the cost of care for the same service can vary widely by location. To try to find out the cost ahead of time – so you can plan for the expense or shop for the best price – experts advise asking your insurance company, since they negotiate the payment rates. (Many insurers offer online cost-calculator tools too.) Before you call, be sure you know the exact procedure or service and, if possible, its billing code. You can also ask your health care provider, although they might not have the negotiated rate as easily available.

A law passed last year aims to make it easier for consumers to learn what their care will cost, but many those provisions don’t take effect for several months. To learn more, click here.

Have a health care topic you’d like some help understanding? Email Mirror health care reporter Arielle Levin Becker at alevinbecker@ctmirror.org.