As legislators fled the Capitol as the coronavirus spread through Connecticut last March, they failed to approve the annual limit on the state’s credit card — a seemingly routine task, but one whose absence now jeopardizes billions of dollars in planned projects.

It’s unclear whether lawmakers will address this oversight later this month when they return to Hartford for a special legislative session, or defer action until after the November elections. Their ability to postpone delivering the bad news ultimately hinges on Connecticut’s cash position remaining strong and having other resources on hand to pay the bills.

“Bluntly, we are ignoring what we know to be the reality of the current situation,” Deputy House Minority Leader Vincent J. Candelora, R-North Branford, wrote recently in a letter to legislative leaders. “The sooner we face reality, the sooner we can start to plan to address this enormous challenge.”

Connecticut borrows billions of dollars annually for capital projects by selling bonds on Wall Street. But there is a borrowing limit and it’s tied to the revenues the state expects to receive each year. As expectations for tax receipts and other resources shrink, so does the debt limit.

Revenue forecasts were high when lawmakers left the Capitol on Wednesday, March 11, to allow for a four-day deep cleaning of the complex. Had the Finance, Revenue and Bonding Committee — before it left — approved a revenue schedule for the fiscal year beginning July 1, the debt limit would have been set high as well.

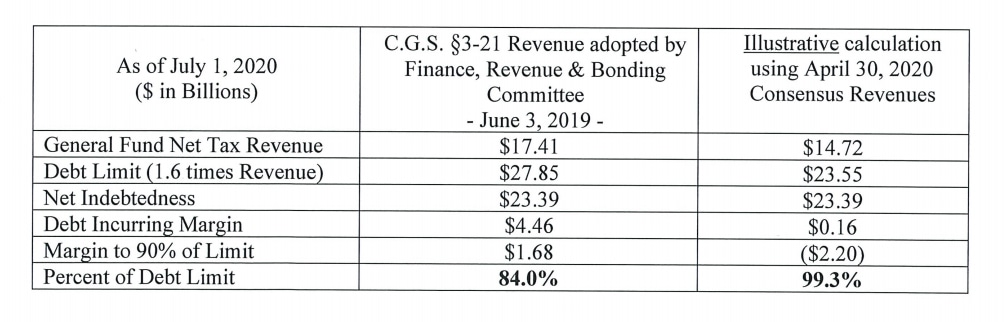

But lawmakers, who expected to return to the Capitol the following Monday, never came back because COVID-19 infections rapidly spread. Leaders indefinitely postponed business, and since then, state analysts have dramatically lowered their revenue projections by more than $2 billion — for this fiscal year and for each of the next two.

Over three years the combined reduction approaches $7 billion, according to an April 30 report. The projections reflect the fact that more than 600,000 Connecticut residents became unemployed as the pandemic shuttered thousands of businesses or forced them to scale back operations.

Some of the revenue drop is temporary. Gov. Ned Lamont deferred income, corporation and other state tax filing deadlines from April 15 until mid-July to assist struggling Connecticut households and companies – a move praised by lawmakers from both parties.

But Candelora said Connecticut, nonetheless, clearly has to scale back its borrowing now.

State law caps not only the outstanding bond debt the state can carry at any given time, but also how much new bonding legislators can tentatively schedule for future approved projects waiting in line to receive financing.

By law, when the state gets within 90% of the debt limit, the governor must craft a plan to immediately reduce planned borrowing below that threshold. If debt exceeds 100%, then all borrowing is shut down.

State Treasurer Shawn T. Wooden warned recently that were the finance committee to adopt a revenue schedule that matched the recent April 30 forecast, Connecticut would be within 99.3% of its debt limit. Lamont and legislators would need to postpone $2.2 billion in planned borrowing to get down to the 90% threshold.

Legislators routinely authorize borrowing for projects months or even years before the state actually borrows the funds to carry them out. The State Bond Commission also has to endorse a project before it is financed, and in some cases, initiatives approved by the legislature never receive funding.

But this doesn’t stop lawmakers from touting the project as soon as the General Assembly gives its OK, particularly if it involves a project earmarked for a legislator’s home district. Nor does it stop Wall Street credit rating agencies from considering these legislative authorizations when assessing Connecticut’s credit worthiness.

Wooden said Thursday that “certain caution is still warranted,” involving the debt cap. “We continue to take careful note of the matter.”

Caution is needed because Connecticut doesn’t borrow money only to finance capital projects. When the state’s cash balance is low, the treasurer may temporarily shift bond proceeds into the common cash pool so the state can pay its operating bills. The treasurer’s office was forced to make several such transfers during the last recession, but Wooden has said Connecticut’s cash position, to date, has been strong.

But if cash reserves run low before the November elections, Connecticut may need to borrow funds. To facilitate that, legislators first would need to reset the state’s debt limit. And to do that, apparently, Lamont and legislators would need to put billions of dollars’ worth of projects on hold — at the worst time from a political standpoint.

Connecticut ranks among the most indebted states, per capita, in the nation, and debt service costs consume more than 10% of the annual budget, a problem that prompted Lamont to press for his debt diet immediately upon taking office in January 2019. To date, though, the governor’s fellow Democrats in the legislature’s majority have balked at that diet.

Chris McClure, spokesman for Lamont’s budget office, said “if the legislature adopts a new schedule, and adjustments are needed, we will work with them to find the best possible solution. If that includes necessary adjustments to bond authorizations, we are able to do so at any time–including in the next regular session.”

But Rep. Jason Rojas, D-East Hartford, who co-chairs the Finance, Revenue and Bonding Committee, said it’s premature to act until Connecticut gets a clearer picture on its eroding revenues, which may take several more months.

“We still don’t have a clear picture of exactly where things stand,” he said. Income tax and other key tax filings are due on July 15, and the state should have a clearer picture of its finances later this summer or early in the fall, Rojas added.

Rep. Chris Davis of Ellington, ranking House Republican on the finance panel, said with Connecticut and the nation sinking into recession, legislators can’t plan to borrow funds taxpayers can’t afford to repay.

“We don’t want to over-extend ourselves in an emergency situation,” Davis said. “We realize the economy is in a deep recession and its unclear when it’s going to lift. It would be unwise of us to continue to spend.”