Many people shopping for health insurance pick plans with the lowest monthly cost. But experts say that’s not necessarily the best buy, since those plans often leave members with steep out-of-pocket costs when they get care.

In some cases, advocates and officials say, people who picked the cheapest options – known as bronze plans – ended up not using their coverage because they couldn’t afford to pay for care.

“Nationally, we are seeing consumers purchasing bronze plans that should not be purchasing bronze plans,” said Jim Wadleigh, CEO of Access Health CT, the state’s health insurance exchange.

So what would make customers take more than the monthly premiums into account when picking plans?

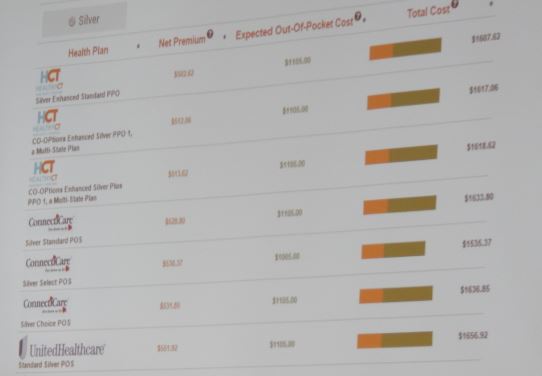

Access Health is developing a tool intended to give customers a fuller picture of their actual costs – both premiums and the costs they would face when getting care, which can vary widely – when shopping for coverage.

The tool is still under development, but is expected to be ready – albeit with room for improvement in future years – for the next insurance open enrollment period, which begins Nov. 1.

As designed, shoppers would enter information – anonymously – about their medical conditions and surgeries they anticipate having. The system would project their likely medical costs under each plan, as well as their premium costs, factoring in any tax credits they qualify for to discount the premiums. For someone with significant medical issues, it might show that plans with higher premiums would nonetheless lead to lower overall costs than a bronze plan.

Access Health officials demonstrated an early version of the tool to members of the exchange’s consumer experience and outreach advisory committee Thursday. Members praised the concept, but suggested a wide range of changes to make it more user-friendly.

Among the issues: how to rid the tool of acronyms and insurance jargon; how to ensure that customers understand the limitations of the tool and how to use it without putting that information in large blocks of text they will gloss over; how to make clear that customers might face higher costs if they see providers not in their plan’s network; and how much nudging the tool should do to let customers know their cheapest option, within legal requirements that it not steer customers to a particular decision.

As part of the federal health law, insurance plans are classified by metal tier – bronze, silver, gold and platinum. In general, plans with the lower tiers tend to have lower premiums but require members to pay more when they get care.

This year, for example, a 40-year-old in Hartford could buy a bronze plan for $222 per month – but would have to pay $6,200 toward his medical expenses before the plan begins chipping in. By contrast, a gold plan would cost $346 per month, but the customer would pay less when getting care – fixed co-payments for most medical services, with a $500 deductible that only applies to certain types of care.

For people with lower incomes, that distinction can be particularly stark because many are eligible for midlevel silver plans with additionally discounted cost-sharing. The silver premiums are higher than bronze plans, but would require the customers to pay significantly less money when getting care. Advocates say many people who qualify for those silver plans have nonetheless purchased bronze plans because of the lower premiums, and ended up avoiding medical care because of the out-of-pocket costs.

Silver plans were the most popular among Connecticut exchange customers in 2014 and 2015, but the proportion of customers picking bronze plans rose in 2015, while the share of silver and gold plans dropped.

The tool is intended to help people avoid purchases based solely on premiums. But Wadleigh offered some caveats: It’s most suited for people who have some familiarity with health care, and might be more difficult for people who are healthy and unfamiliar with health insurance.

“This tool is not going to teach our consumers all the inner workings of health care,” he said, adding that the exchange is also working on broader education for consumers.

The tool doesn’t include all medical conditions; shoppers would be able to choose from about 20 of the most common conditions, as well as about 10 surgeries, and would be able to identify how severe a condition is. The projected medical costs would vary based on a person’s age and gender.

Gerard O’Sullivan, director of the Connecticut Insurance Department’s consumer affairs unit, said the tool should be viewed incrementally. The first version, he said, will be better than the information available to shoppers last year. It will be especially useful, he added, for customers buying plans with help from assisters or insurance agents or brokers.

Because the costs customers would see include both premiums and out-of-pocket costs for care, the numbers would be higher than what people see on the typical shopping screen, which emphasizes the premium. Committee members noted that could bring some sticker shock.

But O’Sullivan said it’s important for people to know the real costs.

“From the education standpoint of insurance, I think those numbers are good for people to know, because that is what the costs are,” he said. “So while the numbers are shocking, it’s telling a story.”