When Connecticut deposits roughly $4.1 billion into its pension funds this fall, it will mark the third consecutive year the state used its budget surplus to whittle down the massive pension debt accrued over more than seven decades.

But a recent analysis from The Pew Charitable Trusts provided a sobering reminder of just how far Connecticut still has to go — even considering its great wealth — to overcome decades of fiscal irresponsibility.

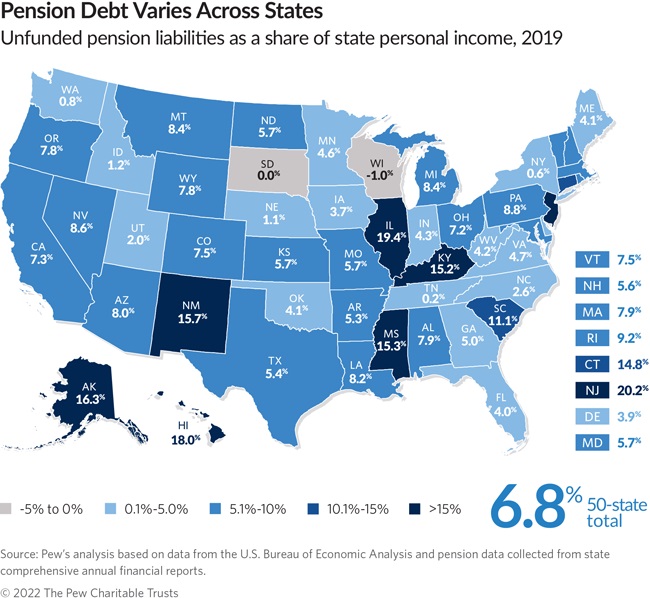

Connecticut had reported more than $41 billion in combined debt among its pensions for state employees and for teachers following the 2019 fiscal year. According to Pew, that represented 14.8% of Connecticut’s personal income at the time — more than double the national average of 6.8%.

Connecticut was one of just 10 states that topped the 10% mark, and ranked eighth-worst overall. New Jersey finished at the bottom with pension debt equal to 20.2% of statewide personal income.

South Dakota and Wisconsin were the only states in which pension assets slightly exceeded obligations.

“Although states have decades to pay off these sums, such spending commitments can have budget consequences both now and later,” Pew analysts Joanna Biernacka-Lievestro and Joe Fleming wrote in their report.

They also noted that “most states continue to face steeper claims on their future revenue from unfunded pension obligations” than from other types of debt, such as bonded debt or insufficient savings for retirement health care benefits.

Connecticut racked up its pension debt over more than seven decades, from 1939 through 2010. And while the state has fully funded its pension obligations since then, it also has refinanced the state employees’ retirement system twice and the teachers’ system once between 2017 and 2019. This involved lowering required payments, both in the late 2010s and in the early 2020s, and shifting billions of dollars in debt, plus interest, onto taxpayers in the late 2030s and 2040s.

Since those refinancings, though, the state has used a robust stock market, surging income tax receipts and a new savings program to amass about $5.8 billion in budget surplus, which it has committed to its pensions in addition to its regular annual contributions.

Besides the $4.1 billion surplus from the fiscal year that closed on June 30, Connecticut also saved $1.6 billion in 2020-21 and about $66 million in 2019-2020.

Gov. Ned Lamont, who inherited the pension challenge when he took office in January 2019, said last month that pension analysts believe these supplemental payments will give Connecticut significant budget flexibility in the near future.

Paying $5.8 billion extra in the pension fund should help to lower required annual contributions to the retirement programs by about $440 million per year.

But there are other forces trying to push the required contributions in the other direction.

The Dow Jones Industrial Average closed Thursday down more than 11% for the year-to-date, and the S&P 500 finished down 15% for the same period.

As the financial markets slip and the value of Connecticut’s pension fund investments shrink, required annual contributions to the system traditionally rise over time.

In addition, more than 4,500 state employees retired between January and June, roughly double the normal number of retirements state government sees in a particular year.

And while Lamont said this “silver tsunami” — driven by new limits on pension benefits starting July 1 — wasn’t as bad as anticipated, any surge in retirement benefits historically puts financial pressure on a pension system. That’s because with each retirement, a worker stops paying into the fund and begins drawing benefits out of it.

Lamont’s budget office downplayed the Pew analysis, calling it an “out-of-date statement of our pension issues.”

Chris Collibee, spokesman for the Office of Policy and Management, added that these supplemental pension payments are “providing stability and predictability to our budgeting and honoring our pension commitments to retired teachers and state employees.”

But the supplemental payments, though unprecedented, still represent less than one-sixth of Connecticut’s long-term pension debt.

And the administration stopped short of predicting those payments alone would put Connecticut’s pension debt on par with the average state, even when measuring pension debt relative to each state’s wealth.

“The pension actuaries will be releasing their valuations of the pension funds later this calendar year,” Collibee added. “While there are many factors that influence the state’s required payments, the additional $5.8 billion in pension fund deposits will bring us closer to the national average as it relates to unfunded liabilities as a share of personal income, and significantly help to address our unfunded liabilities going forward.”