By causing the underfunding of property tax relief grants that are mandated by statute in favor of using “excess surplus” funds exclusively for debt prepayment, the 2017-18 guardrails produced an imbalance in state budget priorities.

Rebalancing the priorities between debt retirement and property tax reduction is one of the principal reasons we urge the General Assembly in its current legislative session to review and readjust the allocation of “excess surplus” before the 2023 guardrail reenactment becomes irrevocable.

Other parts of this series

Authors of the guardrails undoubtedly will claim it is “fiscally irresponsible” to challenge the budget controls. In response, we acknowledge again that these fiscal procedures enacted in 2017-18 succeeded in filling up the Rainy Day Fund and produced significant prepayments of future debt. We hope these positive fiscal practices continue at an appropriate level.

But the authors of the guardrails fail to acknowledge that these positive results came at a significant cost. Our primary concern, as we document in this article, is that making debt prepayments the sole and exclusive priority for using “excess surplus” budget funds has worsened a chronic shortfall in the funding of statutory property tax relief grants.

Here we calculate the statewide cost of lost property tax reductions caused by the guardrails.

How much “excess surplus” was available to fund statutory property tax reduction grants after the Rainy Day Fund had been filled?

The guardrails operate at the end of the budget process primarily to manage what we call “surplus surplus” revenue or what the Office of Fiscal Analysis calls “excess surplus”—that is, fiscal surplus that remains unspent after the state budget has been funded and after the Rainy Day Fund has been filled to its statutory maximum—and divert all of it in an inflexible process exclusively to prepayment of unfunded pension debt.

After the guardrails took effect in 2018, it took several budget cycles to fill the enlarged Rainy Day Fund to its new statutory maximum of 15% of net General Fund appropriations. By the end of budget year 2020, only $62 million could be labeled as “excess surplus” and be transferred to pension debt retirement.

Thus, it was not until the end of budget year 2021 that the Treasurer was required to transfer any substantial Rainy Day Fund balance in excess of 15%– the “excess surplus”—to reduce long-term pension debt. As the chart below shows, the amounts of “excess surplus” to be transferred have been substantial: $1.619 billion in 2021, $4.1 billion in 2022 and $3.2 billion (est.) in 2023.

We stress that these enormous amounts were transferred after the Rainy Day Fund had been fully funded and after the state had already appropriated the Actuarially Determined Employer Contribution (ADEC) for the pension systems.

Our concern is that by sending all of this massive amount of “surplus surplus” to debt prepayment, even if we acknowledge it produces financial benefits, it comes at the cost of blocking state-funded reductions in local property taxes by preventing surplus funds from going at least in part to funding tax relief grants to municipalities.

By how much were existing statutory grants for property tax reduction underfunded during 2021-2023?

To document how this mandatory intercept of the “surplus surplus” blocks reductions in property taxes, the following are three statutory grant programs all impacted in the same negative way.

This analysis may be the first time the amounts of these unfunded property tax reductions have been calculated and acknowledged as a consequence of the guardrails.

- Special Education Excess Cost Grant

The cost of K-12 education, including education for students with special needs, is the largest expenditure in every municipal budget. Special education is an unfunded federal mandate on states and towns that increasingly consumes ever larger chunks of local budgets.

To help local boards of education offset a portion of these costs, the State Department of Education is required to assist towns in paying for services for students with extraordinary needs by providing the statutorily mandated Excess Cost Grant. This grant is intended to provide reimbursement for special education students who require services that in total exceed 4.5 times the district’s average per-student spending for the previous year.

However, the state budget does not always appropriate the full amount of the grant. At times this was because of insufficient revenue, as was often the case prior to 2017. The grant has also been underfunded because the guardrails artificially restrict expenditures even if sufficient revenue has been collected.

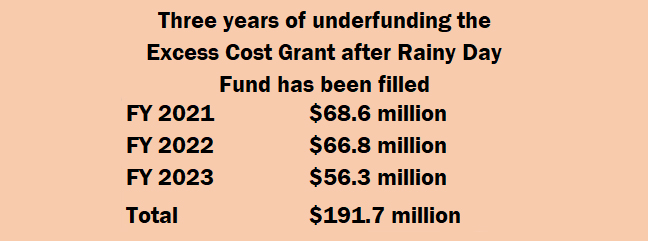

The total amount of the grant for 2022 that should have reimbursed all 169 cities and towns was $207.4 million but the appropriation in the state budget was only $141 million. This meant that property taxes had to make up the $66.8 million difference in the same budget year in which the guardrails diverted $4.1 billion of surplus funds to prepay pension debt.

Thus, the budget guardrails diverted $191.7 million in “surplus surplus” state funds during 2021-2023 from property tax relief that was legally due to cities and towns under the Excess Cost Grant.

- The PILOT Grants

Much the same story can be told about the two major state-funded payment-in-lieu-of-taxes [PILOT] grants that reimburse municipalities for lost property tax revenue due to the exemption from local taxation of state property, private colleges and nonprofit hospitals.

The state has been required by statute to reimburse municipalities for 77% of the lost revenue from private colleges and hospitals, 45% from most state-owned buildings and land, and 100% from land used as correctional facilities.

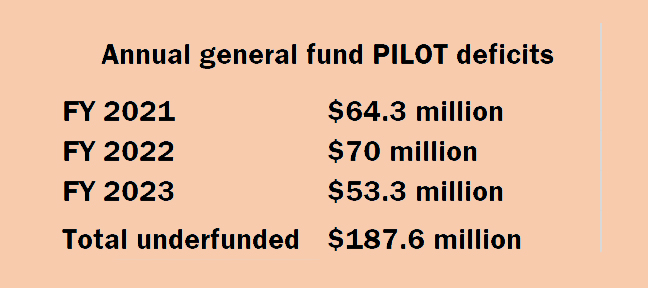

But as with the Excess Cost Grant, the PILOT grants have not been fully funded, leaving the towns to make up the difference in their budgets. In recent years, for example, the state property PILOT grant was funded at an effective reimbursement rate of only 24% and the colleges and hospital PILOT grant was funded at only 33%.

The total general fund underfunding of both PILOT grants for the 3-year period of 2021-2023 when the ‘budget guardrails’ were in place was $187.6 million.

The “budget guardrails” diverted $187.6 million in “surplus surplus” state funds from property tax relief that were legally due under the two largest PILOT grants.

[*NOTE: The General Assembly for FY 22 and FY 23 approved shifting funds from the Municipal Revenue Sharing Account (MRSA) previously promised to municipalities to make up for General Fund deficits in the PILOT grants. These “rob Peter to pay Paul” MRSA amounts are not shown in this chart. The transfers are scheduled to end in FY 24.]

- The Education Cost Sharing (ECS) Grant

The Education Cost Sharing Grant is generally the largest state grant sent to every municipality to help offset the costs of K-12 education. In 2019 the General Assembly adopted a progressive new ECS formula that increased funding to every city and town based on “student education needs” but delayed its full implementation until FY 28 because of the additional expense. Instead, lawmakers adopted an annual “phase-in schedule” to reach full funding by 2028.

The “phase-in” differentiates the shortfall in funding the full ECS formula from the failure to appropriate the full Excess Cost and PILOT grants, but it is similar in that the necessity of phasing in rather than fully funding the new ECS formula was due to fiscal constraints arising largely from the application of the budget ‘guardrails.’

But to the extent that full ECS funding for local education was not made available to municipalities due to fiscal constraints, it is appropriate to cite ECS underfunding and the resulting increase in local property taxes as a consequence of the spending constraints embedded in the budget guardrails that might have been surmounted under a more flexible set of controls.

The following chart shows the differences between what the new ECS grant formula promises to towns if “fully funded” with the actual appropriated “phase-in” ECS grants for each of the fiscal years in which the budget controls have generated “excess surplus:”

The total three-year amount of ECS grant funding that was deferred as a result of the “phase-in” schedule and thus lost to towns for property tax relief is $636.3 million.

- Sufficient “Surplus Surplus” funds were generated in 2021-23 to fully fund the three major property tax grants to municipalities as well as to make the three largest unfunded state pension debt reduction payments in history.

During the 2021-2023 period in which the combination of economic recovery and budget intercepts made available “surplus surplus” funds even after the Rainy Day Fund had been filled, a total of $8.819 billion was deposited in the state’s unfunded pension accounts. During the same period, a total of $1.016 billion was not< deposited in municipal accounts across the state for property tax grants as statutorily required.

Except for the restrictions on the use of “surplus surplus” imposed by the guardrails, there was sufficient revenue generated by the state’s fiscal system during the 2021-23 period that could have been used both to fully fund the three largest property tax reduction grants for the first time in state history and to make the largest three-year deposit ever made of $7.803 billion to prepay unfunded pension debt.

The budget guardrails have not always been the cause of the underfunding of these grants because underfunding was a chronic problem even before the guardrails existed. Historically, both Democratic and Republican governors and state lawmakers have failed to fully fund the grants. Between 2006 and 2020, Connecticut raised only 95.5% of revenue needed to pay its expenses, making it one of only nine states with a 15-year deficit, as it engaged in unsustainable budget maneuvers that allowed pension debt to be deferred and property tax relief grants to go unfunded.

But once the “surplus surplus” revenue became available in 2021, the guardrails became the direct cause of the recent underfunding of the property tax reduction grants because they blocked using any of the “surplus surplus” to fulfill its grant funding obligations.

Tomorrow: How CT’s ‘guardrails’ were transformed into a budget austerity device.

Alex Knopp is the principal author of this analysis on behalf of the following members of the Property Tax Working Group of 1,000 Friends of Connecticut. (Knopp is a former State Representative, Mayor of Norwalk and Visiting Clinical Lecturer at Yale Law School.):

- Bill Cibes, former State Representative, Secretary of Office of Policy & Management and Chancellor of the Connecticut State University System

- Michele Jacklin, former Hartford Courant Political Columnist, Trinity College Media Director and Co-Chair, CT Council on Freedom of Information.

- Jefferson Davis, former State Representative and First Selectman of Pomfret.

- Sue Merrow, former First Selectman of East Haddam and Chair, CT Council on Environmental Quality.

- Albert Ilg, former Town Manager, City of Windsor and Interim City Manager of Hartford.

- Chip Beckett, former Glastonbury Town Council member.