If someone had told me when I left Central Connecticut State University in 2002 that I’d be returning in 2020 and attending classes virtually during a global pandemic, I would never have believed it.

When I left CCSU in 2002, I was juggling a full-time job with the birth of my second child. I told myself that I would someday return to finish what I started and receive a bachelor’s degree in strategic communication. The pandemic provided the perfect time to do that.

Much had changed in my life since 2002, in both my family and profession. I had become a father of three, and professionally, I was in my third year of being the statewide director of active and pension payroll under the state comptroller’s office. My office’s primary statutory responsibility is ensuring that 70,000 full-time and part-time active employees and 65,000 pensioners and optionees are paid on time.

Now, as a 52-year-old student, with two of my children attending the same university, I’ve gained a new appreciation for the words “return on investment.” Unfortunately, a lack of awareness or understanding regarding the return on investment of a college degree can lead some students to make decisions without fully considering the potential economic benefits.

The importance of financial literacy cannot be overstated. From managing student loans to investing for the future, students are expected to navigate complex financial decisions as they transition into adulthood. Yet, the sad reality is that many young adults graduate from high school and college without basic financial knowledge.

This critical gap can be bridged by state universities with a mandatory class on personal finance. The need for such a class is made clear by alarming statistics.

First, two-thirds of American adults cannot pass a basic financial literacy test. A study by the Council for Economic Education found that less than half of states in the U.S. require high school students to take a course in personal finance. As a result, many students enter college with little to no understanding of basic financial concepts. Without proper guidance, they may accumulate credit card debt, make poor investment choices or fail to save for retirement.

Here in Connecticut, Public Act 23-31 was signed into law on July 1. This law requires public schools to build financial management and literacy into their curriculums. The new course will be worth a half-credit and will teach skills like banking, investing, savings, and handling credit and debit cards. This is a small but important step in the right direction.

[RELATED: CT adopts financial literacy requirement for high school graduates]

The second compelling statistic is related to student loan debt. According to data from the Federal Reserve, student loan debt in the United States reached a staggering $1.6 trillion in 2021.

Locally, according to a report from the Office of Legislative Research, Connecticut has the fifth-highest average amount of debt per undergraduate — $35,853, for the class of 2020. Some 15% of Connecticut residents have some form of student debt.

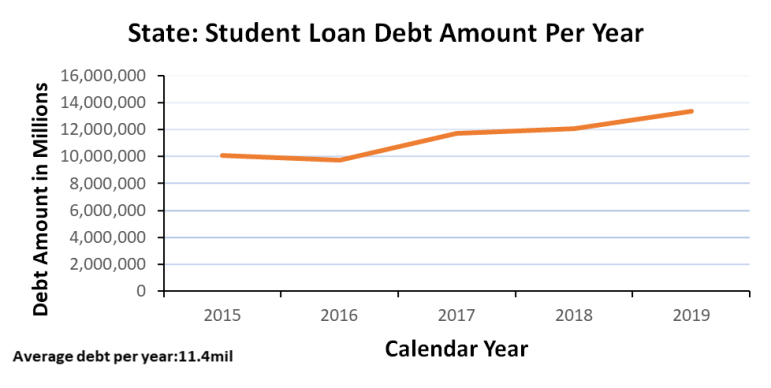

State employees are also feeling the effects of student loan debt. The charts below show the number of state employee student loans and statistics about student loan debt for a five-year period. The state is the largest single employer in Connecticut.

The statistics highlight a concerning trend. A growing number of jobs require a master’s degree, while these same jobs offer annual salaries that are insufficient to justify the financial investment in advanced education.

For instance, consider a graduate who aspires to become a museum curator, a profession that often requires a master’s degree in art history or a related field. While the pursuit of such academic excellence is admirable, the financial reality can be daunting. According to data from the U.S. Bureau of Labor Statistics, the median annual wage for archivists, curators and museum workers is $52,140 in 2020. While this salary might be sufficient for some, it is hardly proportionate to the cost of obtaining a master’s degree, which can range from tens of thousands to over a hundred thousand dollars.

Similarly, to qualify for a “Librarian I” position in the majority of Connecticut municipalities, a master’s degree in library information science is a prerequisite. According to a job posting in the town of Greenwich, the starting salary for a Library I position is $69,652.

The current cost of receiving a library science master’s degree at Southern Connecticut State University, factoring in the cost of a bachelor’s degree, is about $80,000 for in-state commuters. This is assuming the bachelor’s degree is earned within four years. At the national level, only 40.4% of bachelor-degree-seeking students graduate within four years.

In many cases, graduates in these professions may find themselves in a perpetual cycle of debt repayment, struggling to make ends meet.

While the new high school requirement is positive, clearly, one single half-credit high school course will not provide enough knowledge to prevent students from taking on student loan debt or choosing professions that do not justify the financial investment of an advanced education.

I’m in favor of a mandatory personal finance class in Connecticut state colleges and universities to help fill this educational void and equip students with the skills they need to make sound financial decisions. While many colleges and universities offer personal finance courses as part of their business or economic curriculums, I’m advocating for a mandatory personal finance class that would be a prerequisite for every different type of degree.

In addition to addressing financial literacy, universities should tackle the critical issue of this mismatch between the costs of graduate education and the financial returns from specific job prospects. The mismatch could be covered in the proposed personal finance class. The class might propose alternative career options or discuss more cost-effective ways to pursue a graduate degree.

Universities can empower students to make informed financial decisions, avoid crippling debt and pursue careers that align with their financial goals. It’s time for institutions of higher education to recognize the importance of personal finance education and to equip their graduates with the financial knowledge needed to thrive in an increasingly complex financial world.

Mark E. Bissoni, 52, is a fourth-year student at Central Connecticut State University who will be graduating this semester.